The Federal Reserve is Right

Jerome Powell has come under significant criticism. Under closer inspection, the Federal Reserve's decisions are fully driven by economics.

Thank you for reading our work! Nominal News is an email newsletter read by over 4,000 readers that focuses on the application of economic research on current issues. Subscribe for free to stay-up-to-date with Nominal News directly in your inbox:

If you would like to support us in reaching our subscriber goal of 10,000 subscribers, please consider sharing this article and pressing the like❤️ button at top or bottom of this article!

According to multiple news sources, the Republican administration has recently considered removing Chairman Jerome Powell from his position at the Federal Reserve. This recent rise in tension between the government and the Federal Reserve stems from the idea that the Federal Reserve should lower interest rates in the US in order to stimulate the economy.1 The main disagreement between the Federal Reserve and the government revolves around the effects of tariffs on the economy and the appropriate response of a central bank. Let’s discuss why the Federal Reserve is right.

Tariffs and Inflation

The Federal Reserve is concerned that tariffs can result in higher inflation, while the government believes this is not true. The key argument made by tariffs advocates can be summarized in four points:2

Tariffs are not inflationary, because they are only one-off price increases.

Other prices will adjust to offset the increased cost of tariffed goods.

Economists wouldn’t say other taxes, like carbon taxes, are inflationary.

If we look at the recent inflation data, inflation hasn’t gone up.

Let’s unpack these points.

Regarding the first point, it is worth noting that even a one time upward shift in the overall price level is inflation. However, I understand that the focus of this statement is whether tariffs can lead to persistent inflation. To answer this question, we need a model.

Modelling the Impact of Tariffs

Long-time followers of our newsletter are likely familiar with the New Keynesian model, which we have covered in great detail. This model serves as the primary framework utilized by central banks to understand inflation dynamics.

The main implications of this model are that inflation is directly related to the real marginal cost, where the real marginal cost is how much it costs to produce one more unit of an item in real terms.

Tariffs on intermediate goods like steel or raw materials directly impact the real marginal cost; these tariffs increase the expense of producing items domestically that rely on these taxed goods. If nothing else changes, these tariffs will push inflation higher.

But Not Everything Stays the Same – Relative Price Adjustment

Since central banks target a particular inflation rate, they may respond to the prospect of higher inflation by adjusting interest rates. Increasing interest rates dissuades business formation and investment, leading to a decrease in hiring and a rise in unemployment. Increased unemployment undermines workers' ability to negotiate wages, resulting in a decline in their real wages. When real wages decrease, the actual marginal cost of production also falls, which contributes to lower inflation.

The central bank is essentially navigating a trade-off between inflation and a declining labor market. Typically, both things will occur. This brings us to the second point – ‘other prices will adjust to tariffs’. Unfortunately, the ‘price’ that adjusts in response to tariffs is wages as described. Thus, anyone emphasizing the relative price adjustment is, knowingly or unknowingly, saying that wages will go down.

This is actually the biggest cost of tariffs. Model estimates suggest that the impact of tariffs on real wages will be 5 times greater than inflation (a 0.5 percentage point (pp) increase in inflation, but a 2.5pp fall in real wages).

Are Other Taxes Inflationary?

The third argument made by tariff-inflation skeptics is the claim that other taxes, like carbon taxes, would not cause inflation.

First, this isn't true. Research tells us that carbon taxes will be inflationary – Moessner (2022) shows that a $10 charge per ton of emitted CO2 would result in about a 0.1pp increase in inflation.

Second, the reason the impact of carbon taxes on inflation would be muted is that there are low/non-carbon alternatives that are exempt from the tax (for example, renewable energy). Thus, producers have alternatives and can mitigate some of the carbon tax.

In the case of the current tariff implementation, firms lack easily accessible alternatives since the tariffs are applied universally on almost all countries and all goods. Thus, producers will face a larger production cost, resulting in higher inflation. Moreover, anticipating that inputs sourced from the US could serve as alternatives is unrealistic, given that the US itself has limited spare production capacity.

We Haven't Seen Inflation Go Up

The last common argument about tariffs and inflation is that inflation has not risen since the introduction of tariffs.

Firstly, we have seen inflation go up due to tariffs, as we discussed here.

Secondly, it’s also important to understand how much of an impact tariffs can have on inflation. As discussed here, we should not expect inflation to be impacted by more than 0.5 to 0.8 percentage points by tariffs. That's because goods trade is a relatively minor part of the US economy, accounting for about 14% of GDP. No economist would say that tariffs would cause a big inflationary jump and it would be foolish to try to discern the tariff impact just by looking at the headline numbers.

Lastly, the US tariff policy is currently constantly changing, which makes even establishing the effective tariff rate basically impossible (the Yale Budget Lab aims to estimate this number). Without knowing the actual effective tariff rate, it is also difficult to estimate by how much inflation will fluctuate.

Federal Reserve Decisions

The above discussion is meant to illuminate how to think of the impact of tariffs on inflation. The Federal Reserve is aware of these models and research. The tariff uncertainty creates a conundrum for the Federal Reserve, as it does not know how large and for how long the tariffs will be enacted. We previously discussed that under the April 2 tariffs schedule, compared to a world with no additional tariffs, the optimal policy by the Federal Reserve would be to allow for 0.5pp to 0.8pp of extra inflation, with interest rates also being higher by this amount.

The Federal Reserve is right in being hesitant to change its policy stance – tariffs can push inflation up, and adopting a wait-and-see strategy seems prudent, as long as the uncertainty around tariff policy remains.

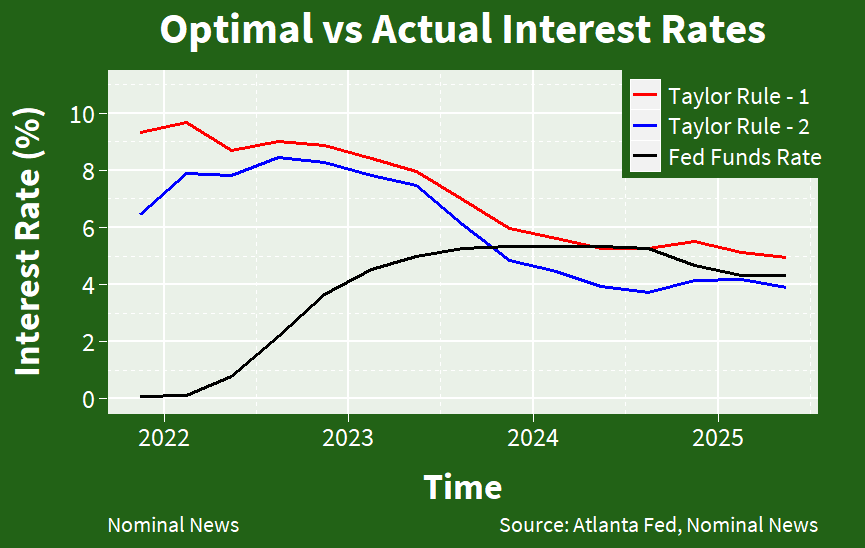

An “Automatic” Interest Rate Rule

Separately, since interest rate policy is often set in response to economic variables, some have proposed using a mathematical formula for it. One formula, often used by economists, is the Taylor Rule proposed by economist John B Taylor. This formula computes the optimal interest rate using data on inflation and economic output. While the Federal Reserve does not officially adopt this rule for policy-making, its decisions often align closely with it. Interestingly, depending on certain modelling assumptions within the Taylor Rule, today the formula would suggest an interest rate between 3.9% and 4.9%, which is very similar to the current interest rate of 4.25%-4.50%. This approach also suggests that the Federal Reserve is right in holding the interest rates as is.

The black line is the actual interest rate policy of the Federal Reserve, while the blue and red ones are the ‘optimal’ interest rates based on the Taylor Rules under different specifications.

Interesting Reads from the Week

Article: Claudia Sahm talks about the issue of Federal Reserve independence and how it’s related to the budget of the Federal Reserve.

Article: Dave Deek highlights a problem with government policies that increase the retirement age, as these may policies may have significant adverse impacts on youth employment.

Article: For All, a newly launched Substack by Sean, PhD student economist, talks about how special economic zones contributed to the large economic growth in China.

Lower interest rates increase spending (as it is less beneficial to save) and also make opening up new business cheaper as loans cost less.

The other two key components for inflation in the New Keynesian model are desired mark-up (the economy-wide profit firms are targeting) and expected inflation (what market participants believe inflation will be in the future).

"If the administration follows through on its goals of deporting 4 million people over four years:

There will be 3.3 million fewer employed immigrants and 2.6 million fewer employed U.S.-born workers at the end of that period.

Employment in the construction sector will drop sharply: U.S.-born construction employment will fall by 861,000, and immigrant employment will fall by 1.4 million.

The deportations will eliminate half a million child care jobs." - economic policy institute

How does the model intrepret this? Even if the total is half of this projection, there will be less available workforce participation and won't this INCREASE wages as there is a potential shortage of workers?

Thoughts?

Very interesting article, thank you.

I read another interesting article on this from Derek Thompson substack.

One argument he makes is that inflation is not going up as much as expected, amongst other things, because the Fed is keeping interest rates up.

Reminds me of a friend of mine, who had a really nice figure, but was always dieting. I once said to her that I didn't understand why she was always on a diet, given her very nice figure. She replied, "and I have a great figure because I watch what I eat."

Another person keeping track of tariffs and demonstrating how they are continuously being changed is Joey Napolitano, also on substack. Tariffs are shifting frequently, sometimes being lifted soon after being announced, this mitigates their overall impact. I mean, who can keep track anymore?