Economic Friday – Interpreting Tariff, GDP and Inflation News

Friday, February 20, was a big economic news day, with the Supreme Court ruling on tariffs along with data releases on GDP and inflation.

Nominal News is an economics newsletter written by a PhD Economist that translates the latest economic research into clear, policy‑relevant insights on current issues. Join 4,000 readers for free to stay-up-to-date with Nominal News directly in your inbox:

Friday, February 20, 2026 was a big economic news day in the US.

The US Supreme Court deemed President Donald Trump’s tariffs issued under the International Emergency Economic Powers Act (IEEPA) as illegal.

The Bureau of Economic Analysis (BEA) published US fourth quarter Gross Domestic Product (GDP) data which showed that real GDP growth was 1.4% (while various official forecasts were suggesting between 2.5% to 3.5% growth).

The BEA also released the Personal Consumption Expenditure Price Index (PCE – the Federal Reserve’s preferred measure of inflation) for the month of December, which showed inflation at 0.4% (month-over-month) and 2.9% (year-over-year).

So how do all these pieces of news fit together?

Tariffs – Soon to Disappear?

The decision by the Supreme Court to deem the tariffs as illegal was widely expected. But this doesn’t mean the end of tariffs, as President Trump quickly reinstated tariffs under a different section of US law. The newly announced tariff rate – i.e. tax rate on imported goods – is 15% on all imports, regardless of origin. These new tariffs can only be in place for 150 days until Congress must approve them through a vote. At the same time, the legality of these tariffs is also being questioned.

The exact impact of the recent changes in tariffs is still ambiguous. Some are forecasting a higher effective tariff rate than was currently present (the effective tariff rate is computed as the total amount paid to the government by importers over the total amount that is imported). On the other hand, the Yale Budget Lab estimates that the effective tariff rate will be lower. Nonetheless, there will definitely be a change in the distributional impact of these tariffs, since the new tariffs are placed on all countries, while the previous tariff regime was targeted at different countries.

Tariff Refunds?

One significant development emerging from the Supreme Court decision is whether the tariffs collected in 2025 will need to be refunded to the importers. From an economic perspective, if the tariffs are refunded, it may lead to the net impact of the tariff policy being a large transfer from consumers to firms.

To understand why, we first note that tariffs are simply a tax on imported goods paid by US based importers. This tax, however, is ultimately paid by local consumers since importers typically increase the price of these imported goods in the US to recoup the tariff (tax) they had to pay. Now, the benefit of this tariff (tax) is that the government (i.e. US citizens) gets the revenues. With the Supreme Court ruling, if this collected revenue gets refunded, it will go back to the importers, since they were the one that paid the tariff tax originally.

Therefore, the net impact of these IEEPA tariffs with the Supreme Court ruling could be a de facto transfer from local US consumers to US importing firms, making it a very regressive policy (transferring from poorer individuals who had to pay extra for goods to richer individuals – owners/shareholders of importing companies).

However, it is worth adding that even absent these potential refunds, the tariffs have adversely impacted GDP growth and increased inflation.

GDP Growth – Negative Impacts of Tariffs

US fourth quarter real GDP growth came in at 1.4%, which was lower than various forecasts suggested. It is worth adding an important caveat. One of the reasons real GDP growth came in lower than expected was due to the government shutdown that lasted 43 days (October 1 to November 12, 2025).

Aside – Government Services Adjustment

Government-provided services are part of GDP. During the government shutdown, the government stopped providing most services, so in calculating total GDP, it can be assumed that the government provided 43 days less worth of services. But at the same time, government employees were still paid for these 43 days. Therefore, during the fourth quarter, the US government provided fewer services, but it cost the exact same amount as in other quarters during the year.1 Thus, although nominal GDP came in at 5.1%, real GDP came in at 1.4% since the amount of real government services was 43 days fewer.

Absent the government shutdown, the fourth quarter real GDP growth would have been closer to 2.5%. This ‘missing’ real GDP will reverse in the first quarter of 2026, as the government will return to a normal level of government service provision.

Overall 2025 GDP Growth

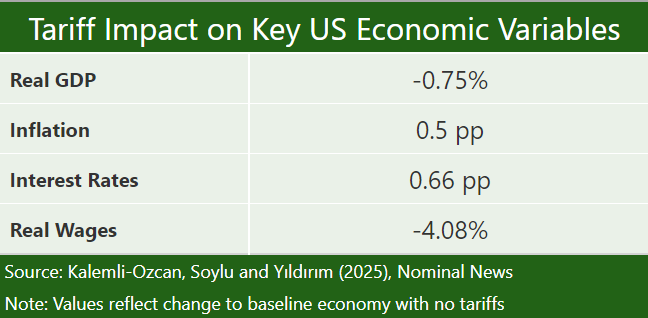

For 2025, real GDP growth was 2.2% (adjusting for the government shutdown, it would have been 2.5%). In 2024, real GDP growth was at 2.8%. Last year, we wrote an article talking about research on the likely impact of tariffs, summarized in the table below:

The above table shows that tariffs were estimated to lower real GDP by around 0.75% in the period after tariff enactment. Interestingly, this means that absent tariffs, real GDP growth in 2025 would have been around 3.3% (after adjusting for the government shutdown and adding the impact from the table), which would be a bit higher than 2024 real GDP growth.

Although this high level comparison is not definitive, it does appear that these initial estimates in the Kalemli-Ozcan, Soylu and Yıldırım (2025) have captured reality well. Even the inflation forecast seemed quite good.

US Inflation

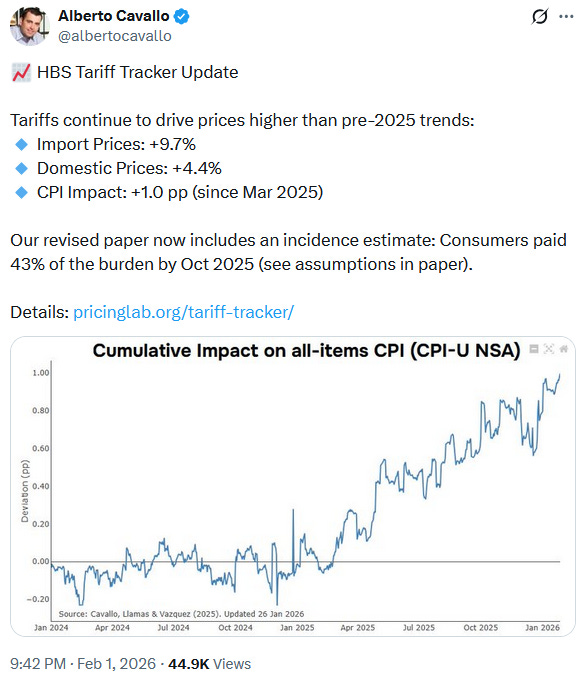

After the release of the December data, US PCE measured inflation for the year was 2.9%. Using the estimate in the table above, absent tariffs, inflation would have probably been around 2.4% (target inflation is ~2%). Some data suggests that inflation may have been even lower absent tariffs. The image below shows a different estimate:

Since March 2025, Consumer Price Index (CPI) measured inflation (a slightly different inflation measure) would have been 1 percentage point lower had tariffs not been enacted.

Tariffs and the Economy

The recent developments show us that tariffs (a domestic tax on imported goods) are really not a good policy. So far, tariffs:

Led to higher inflation by around 0.5 pp to 1 pp;

Reduced GDP by around 0.3%-0.5%; and

May end up being a direct transfer from poorer consumers to richer importers.

I think it’s safe to say that these are not generally desirable outcomes from a policy perspective.

The only positive from this tariff policy is that it has shown that academic economists are pretty good at modelling the impacts of such a policy, and, perhaps, they should be listened to a bit more.

To read more on our coverage of tariffs:

Yes – Tariffs Have Increased Prices and Inflation in the US (June 15, 2025)

Modelling the Impact of Tariffs (April 30, 2025)

Why Import Tariffs are Identical to Export Taxes (April 13, 2025)

Do Tariffs Cause Inflation? Yes. (March 24, 2025)

If you would like to support us in reaching our subscriber goal of 7,000 subscribers, please consider sharing this article and pressing the like❤️ button at top or bottom of this article!

Interesting Reads from the Week

Trust in Numbers – Claudia Sahm tackles the concerns around the reliability of US government statistics, showing that the statistics are currently reliable, although funding cuts may make collecting data harder.

Removing Truth & Sanity from American History (United States) – Keshler Thibert conducts an interview with Michiko Quinones (Co-Founder and Director of Public History for the 1838 Black Metropolis Project), where they discuss the re-writing of history via the recent removal of display panels from the President’s House in Philadelphia, which included information about the role of the U.S. slave trade in the development of the country.

America’s Pensions Can’t Beat a Vanguard Account Or Finance a Transmission Line, But They Can Close Your Hospital – Dave Deek discusses how pension funds can invest in important projects for society (energy projects, additional housing). Pension funds in other countries often do this, while US pension funds appear to be less efficient with their use of capital, spending a lot more on fund managers.

The same cost for fewer services is basically inflation.