Jerome Powell – A Look-Back at a Great Federal Reserve Chair

It's important to give credit where it's due – Jerome Powell steered US monetary policy very well.

Nominal News is an economics newsletter written by a PhD Economist that translates the latest economic research into clear, policy‑relevant insights on current issues. Join 4,000 readers to stay-up-to-date with Nominal News directly in your inbox:

On May 15, Jerome Powell, who had been serving as the Federal Reserve Chair since February 5, 2018, was officially replaced by Kevin Warsh. His legacy as the head of the Federal Reserve will always be defined by the handling of the tumultuous time period that involved one of the largest economic shocks – the Covid pandemic. In my opinion, Jerome Powell was a great Federal Reserve Chair, and not just because of how he steered the US through the Covid shock.

.jpg")

“Covid” Shutdown and Inflation

The Covid pandemic led to an unprecedented global economic shutdown. The US unemployment rate jumped by 10 percentage points in one month and would have been much higher had it not been for certain government measures that incentivized keeping workers ‘employed’ like the Paycheck Protection Program (known colloquially as PPP loans).

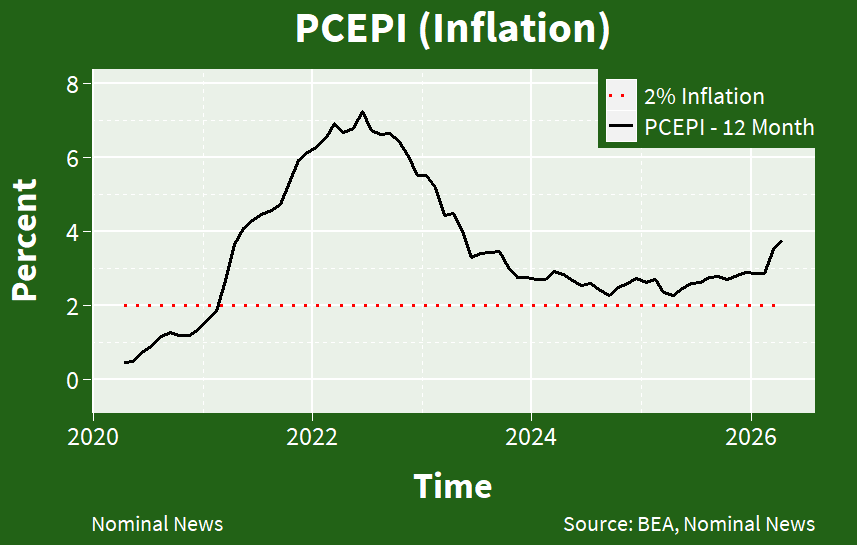

To support the economy and prevent any recessions, the Federal Reserve under Jerome Powell kept interest rates at 0%, purchased assets to free up liquidity, as well as extended various loans to financial institutions and municipalities. Without a doubt, both fiscal and monetary policies kept the US economy afloat and the recession that did occur was extremely short-lived. However, this came with a cost – elevated inflation:

This elevated inflation is the main criticism levied at Jerome Powell. However, I believe Jerome Powell, and the other members of the Federal Open Market Committee, were correct in the way they dealt with the Covid economic shock.

We have previously discussed the Federal Reserve’s handling of the Covid shock in depth, so I will only briefly touch upon the discussion by highlighting two key points:

Inflation during the Covid pandemic may have been mis-measured due to the uniqueness of the Covid shock;

The best response to a ‘supply-shock’ like the Covid shock, was to run the economy ‘hot’ (generating inflation).

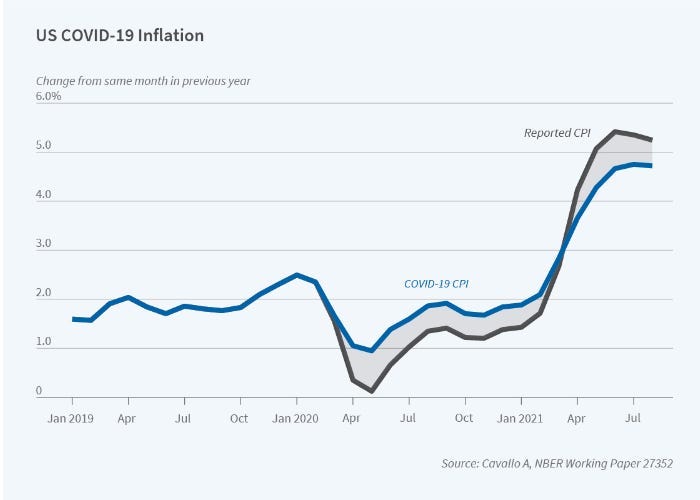

Regarding the first point, I will point to our “Causes of Current Inflation” article and the Cavallo (2021) paper, which argued that consumers drastically changed what they were spending on during the pandemic. If we were to correct for the consumption patterns of consumers, initial inflation during the pandemic was under-stated, while later inflation was over-stated:

The blue line is the adjusted inflation, while the grey line is the official inflation data. This means that peak inflation towards the end of the graph was probably a bit lower during the Covid shock (even though cumulative inflation was the same).

Regarding the second point, quoting from our previous article:

“During the COVID pandemic, due to safety precautions, many businesses were often forced to temporarily shut down due to lockdowns or had to alter their production methods to satisfy social distancing and capacity requirements. This naturally increased the real cost of production – for example, what may have previously taken 10 hours to make would now take 12 hours to make. This increased real marginal cost is directly linked to an increase in the rate of inflation (which we have discussed in depth here).

The optimal policy by the Federal Reserve to address the supply shock-driven inflation surge, as discussed by Lorenzoni and Werning (2023), can be to run the economy ‘hot’ (i.e temporarily have the economy produce more than its long-run potential) while the supply issues resolve, which results in inflation to continue to be higher than target. At the same time, in a ‘hot’ economy there is greater labor demand as businesses keep expanding, which allows for workers’ wages to catch up. The ‘hot’ economy also helps resolve some supply issues, as it encourages more business to form, alleviating the supply issues.

My Opinion: Given inflation surged right after the pandemic, it appears that the Federal Reserve did run the economy ‘hot’. Whether this was a deliberate decision or not, from an optimal policy standpoint, this decision appears to be correct. The Federal Reserve, in my opinion, acted well.“

Did the Federal Reserve Do Too Much

If one agrees that the Federal Reserve was correct to stimulate the economy, a legitimate question is did the Federal Reserve stimulate too much, which resulted in much higher inflation than was potentially needed to offset the Covid shock. This is a hindsight-type question, making it subjective in nature.

If we knew at the onset of the pandemic in 2020 how exactly it would progress, then we could argue that the Federal Reserve should have not stimulated the economy as much as it did, and the Federal Reserve perhaps should have increased interest rates earlier. But, this framing ignores the uncertainty that we had during the Covid shock.

What if the Covid pandemic turned out to be a much larger economic shock, keeping business closed much longer? What if more aggressive strains of the virus were to evolve? Ultimately, the Federal Reserve had to make a decision under this uncertainty. So I don’t think it makes sense to judge the Federal Reserve decisions based on how the Covid pandemic developed, but, rather, it should be judged based on how the Covid pandemic could have evolved.

For example, if economic lockdowns lasted several months longer, would the Federal Reserve decisions have been appropriate? Perhaps if they didn’t stimulate the economy as much as they did, under this worse Covid scenario, a deeper recession would have occurred. Thus, the way the tenure of the Federal Reserve should be judged is by looking whether the Federal Reserve decisions were targeting a worse Covid scenario than the one that occurred.

The Federal Reserve may have erred on the side of preventing an economic recession at the expense of higher inflation, which occurred as Covid turned out milder. In the words of New York Knick and NBA champion, Jalen Brunson – “You’re allowed to think about the worst-case scenario, but you gotta go out there and do something about it.” The Federal Reserve chose to do something in case the pandemic turned out much worse.

Overall, I believe the Federal Reserve under Jerome Powell acted reasonably and well. Arguing that the Federal Reserve should have made better decisions is tainted by hindsight bias.

An Open-Minded Federal Reserve Chair

The main reason I found Jerome Powell to be a good Federal Reserve chair is his general openness to discussion and ideas. He was also very transparent in how he was thinking through the various economic shocks. For example, here’s a quote from his March 2026 press conference on how he was thinking about tariff inflation:

“...when tariffs are put into place, of course what they do is they raise prices to some extent… It takes 8, 9, 10, 11 months—a year— to go through the system. And we’re waiting for the tariffs, which were put in place over the course of the middle part and later last year, we’re waiting for that to go through the system so that goods inflation will return closer to what it’s always been. I mean, it used to be—for many, many years [goods inflation] was negative, and then the year before tariffs came in it was zero. And … goods inflation is [currently] running at 2 percent.”

Powell clearly states how he viewed the impact of tariffs on inflation.

“But we’re not seeing progress there. … what we want to see for this year, rather, is continued progress on housing services, finally seeing the goods inflation come back down, because the one-time effects of tariffs are through, and then also get some help from nonhousing services. That’s what we’d like to see. But it’s, you know, it’s a good question why we didn’t see much of [non-housing services inflation coming down] last year.”

It’s also worth pointing out that Powell’s level-headed approach to data has been vindicated recently. For example, in the March 2026 press conference, a journalist presented a question that suggested the labor market is doing worse and perhaps rate cuts were needed:

“Journalist: So in December we saw employment numbers revised down to negative 17,000, January revised down, February posted a loss of 92,000….is the employment side a far greater risk than the inflation side? Because we are seeing inflation—CPI is close to 2 percent, PCE has ticked down overall

Powell: … I wouldn’t say that that’s clear at all, that one is more at risk than the other. …you can point to the unemployment rate being stable, and in a world where both supply and demand for workers have come down very, very sharply over the course of the past year due to immigration policy largely, you know, a ratio is going to be a better thing to look at than job creation, for example. And the ratio is the unemployment rate, and it’s been stable since September…. …we’re at 3.0 percent core inflation, 2.8 percent headline, so we’ve been well above 2 percent, that amount, whatever it is, 0.7, 0.8, we’re a full percentage point above 2 percent for some time. And that’s a concern. We need to get back down to 2 percent. And we need to keep focused on that, even though we do now face some new inflation from energy. So I’d be hard pressed to say that one of them is obviously more at risk than the other.”

Given that in May we saw employment grow by 172,000, unemployment remained stable, while inflation was elevated, Powell was again correct in his nuanced take.

To me, Jerome Powell appeared to be an inquisitive and open-minded person, listening to the different strands of research. In the above quote, for example, Powell acknowledged that immigration policy may explain why we are seeing lower job creation numbers, something highlighted by Guy Berger here. Jerome Powell stayed very close to fresh economic research, and this type of approach is something a Federal Reserve Chair should have.

Jerome Powell is a great example of what an economist should be. And, what may be surprising to some, Powell does not have an economics degree (he has a law degree)! However, Powell demonstrates that, in essence, economics is a formalized approach to thinking about social issues, and that anyone, even without formal economics training, can be a good economist. This is something I strongly believe in (and hope to convey with Nominal News).

For this reason, I found Jerome Powell to be a great Federal Reserve Chair.

P.S. Kevin Warsh – the New Federal Reserve Chair

The most recent Federal Open Market Committee on June 17, 2026 was chaired by Kevin Warsh. I covered this meeting, as well as the press conference with Kevin Warsh in a special edition article here. I found his press conference quite concerning, and, in many ways, the opposite of the openness and clarity of Jerome Powell. We are in for some interesting times.

If you would like to support us in reaching our subscriber goal of 7,000 subscribers, please consider sharing this article and pressing the like❤️ button at top or bottom of this article!

Appreciating your learned comments I believe you omitted the most important reason why Powell should be seen as a Great Chair. His short statement about the FED independence is among the crucial moments in the FED relation to the Executive.

The more poined question is did the Fed start reining in inflation soon enough? What would l have happened if it had raised rates in Sept 2021 (when TIPS rose > target) and or started more vigouous QT instead of march 2022?

Also, instead of just "predicting" that inflation would be temporary, the Fed could have committed to _making_ it temporary. It never quite escaped the "Fed fighting inflation" (and temporarily loosing the fight) syndrome, instead of saying outright that it was engineering temporary inflation to facilitte adjustment of relative prices to the COVID shock and would stop it at the right time.