Special Edition: Federal Reserve FOMC Meeting Update

On June 17, 2026, the FOMC met for the first time with Kevin Warsh as Chairman.

Nominal News is an economics newsletter written by a PhD Economist that translates the latest economic research into clear, policy‑relevant insights on current issues. Join 4,000 readers to stay-up-to-date with Nominal News directly in your inbox:

Summary

The FOMC (the interest rate setting committee) decided unanimously (12-0 vote) to keep interest rates between 3.5% and 3.75%.

The FOMC also released their projections for the economy, inflation and interest rates.

Commentary

The Decision

The decision by the FOMC to keep rates steady should not be surprising. Current forecasts for May 2026 place 12‑month inflation at 3.4% for core (excluding food and energy) PCE (Personal Consumption Expenditure) and 4.1% for headline PCE. On a month-to-month basis, Core PCE inflation is expected to be up in May by 0.35%, which annualizes to an even higher inflation rate of around 4.3%. At the same time, unemployment has not increased significantly, although real wage growth has turned negative in the recent months. Unfortunately, the main way higher interest rates push inflation down is by lowering real wages.

What was perhaps more surprising is that the vote was unanimous - all 12 FOMC voters chose to keep the interest rate the same. We didn’t see a dissent either way - no voter wanted to increase or decrease interest rates. This does suggest that Kevin Warsh himself appears unlikely to cut interest rates pre-emptively. At the same time, we may have expected certain voters to advocate for an increase in rates.

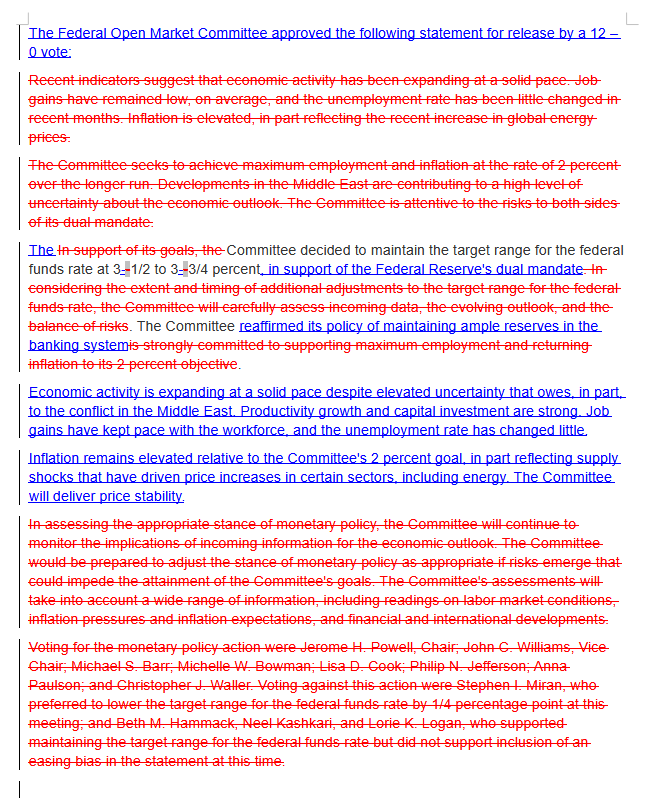

The Statement

Below is the changes of the FOMC statement from April 2026 to today:

As you can see, the statement has been entirely rewritten and the amount of information contained in it is much smaller. There are few glimmers of what the discussions focused on in the FOMC meeting, as referenced by the comments on productivity and capital investment. Both of these elements, however, are not necessarily the most relevant to the current inflation level, suggesting a shift in priorities

FOMC Forecasts

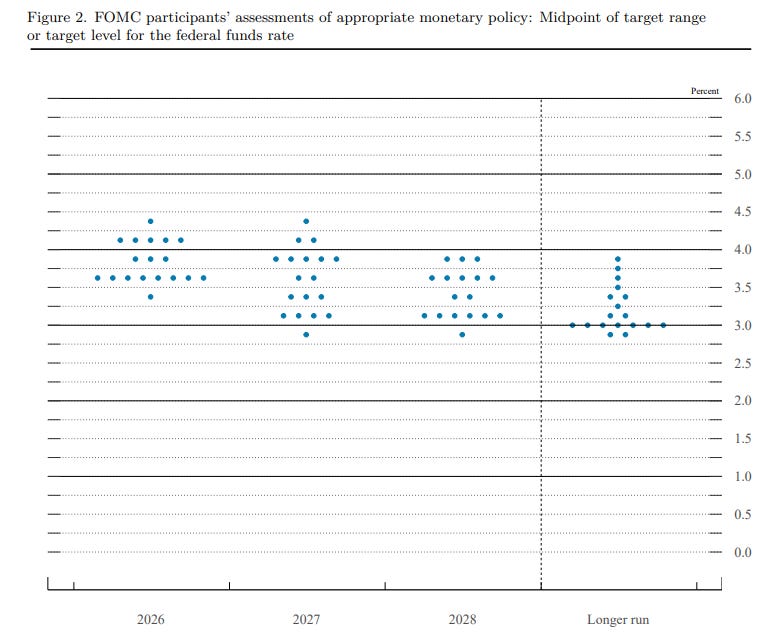

The FOMC also published its views on the economy, commonly referred to as the “Fed Dot Plot”. Basically each member of the FOMC states what they believe the economy will look like in the next few years.

The main point of note is where the committee members believe the interest rates will be:

The above chart tells us that for 2026, 1 member believes there will be a cut (the dot between 3.25% and 3.5%), 8 believe in no change, while 9 believe a rate hike will be needed!

To me, this is not surprising, as inflation is pretty clearly too high and there are concerns that the elevated inflation could entrench itself.

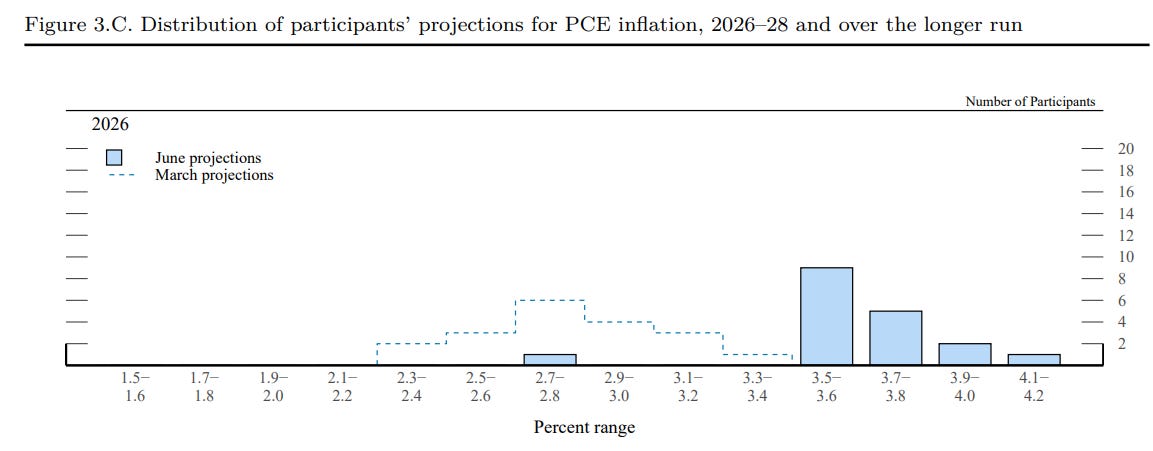

It is also worth seeing how the FOMC participants perspective on inflation changed for 2026:

The dashed lines are what FOMC participants believe inflation would be in 2026 as of March 2026. The blue columns is what the participants currently believe.

Kevin Warsh Press Conference

Kevin Warsh had his first press conference - and it was definitely interesting, as well as concerning.

Forward Guidance

WIth the above FOMC statement and the press conference, Kevin Warsh was clear that he will not provide forward guidance. Forward guidance is the practice of signalling how the FOMC may make decisions in the future. To give an example, one question that Kevin Warsh was asked was how long is he comfortable seeing inflation above the 2% target. His response was that he will not give forward guidance. Kevin Warsh’s push against forward guidance is so determined that he also did not submit his own projections in the “Fed Dot Plot” above.

This is a significant change from past behavior of the FOMC, and I believe it’s for the worse. Central bank transparency is generally a stabilizing force, as it informs market participants what to expect. Less transparency does not feel like a good approach, and we should expect increased uncertainty.

Task Forces

Another big announcement from Kevin Warsh was the creation of 5 different task forces inside the Federal Reserve. These were:

Fed Communications;

Fed Balance Sheet;

Data Sources;

Productivity and Jobs;

Fed’s Inflation Frameworks

The ones that appear most interesting (and concerning) are the focuses on communications, data gathering and inflation frameworks.

Communications - this has already been changed, as discussed above, with much shorter statements and no forward guidance. Kevin Warsh also intimated that even the “Fed Dot Plots” may be suspended in the future. Whether the communication task force will actually improve communications is to be seen, but so far this looks somewhat worrisome.

Data Collection - this task force sounds good on paper, but again there are concerns. It is worth noting that economists have studied monetary policy extensively, and thus have examined a wide range of data and data sources. Kevin Warsh mentioned that he wants more ‘real-time’ data rather than lagged data. However, ‘real-time’ data is often not particularly accurate. At the same time, interest rate changes impact the economy slowly and thus the need for ‘real-time’ may not be as warranted. An example mentioned by Kevin Warsh was the Employment Situation Summary, where he criticized the fact that the numbers get revised several times. The concern here for me is that Kevin Warsh appears to overestimate how precisely one can measure a labor force of roughly 160,000,000 people. Revisions of 100,000 or 200,000 are minuscule.

Inflation Frameworks - this task force appears to be very vague, as it aims to focus on what ‘drives inflation’. Many economists study monetary policy and inflation. It’s a bit surprising that a task force would be expected to outperform the extensive research already available. This does not appear to be a project for a task force.

Big Changes Coming and Not Necessarily for the Better

Although rates remained the same, this FOMC meeting pointed to very large changes, which sound somewhat concerning. I don’t think reduced Fed communications are likely to improve monetary policy outcomes. The task forces on data and inflation frameworks might sound good on paper, but also do not really appear to be helpful (especially since we do not know yet who will lead them).

Overall - interesting times are coming to the Federal Reserve.

Let me know what you think about the new Federal Reserve Chairman’s comments.

This has been a special edition Nominal News article covering a very recent development. Please let me know your thoughts on this feature, and what would you like to see covered, in the comment section below.

If you would like to support us in reaching our subscriber goal of 7,000 subscribers, please consider sharing this article and pressing the like❤️ button at top or bottom of this article!

More detail:

“Unfortunately, the main way higher interest rates push inflation down is by lowering real wages.”

I disagree. Interest rate increases, ceteris paribus, reduce aggregate demand. That does not necessarily slow wage growth more than product price growth. Your statement more likely applies in a one good, one (labor) input, one relative price (real wages) model.

“Central bank transparency is generally a stabilizing force, as it informs market participants what to expect. Less transparency does not feel like a good approach, and we should expect increased uncertainty.”

Another disagreement. Your statement conflates predictions (guidance) about future policy instrument movements, with guidance about what outcomes the Fed is seeking. (I share your concern about the _content_ of the guidance, but that is a separate issue.)

Task forces:

Communications: I’ve had my say

Data: Agree that Walsh sound mixes up here. But boy are there data issues that could be improved! He should get his buddy, Bessent to create new, shorter tenor TIPS and start issuing a Trillionth, a security that pays a percent of future GDP. Also, the Fed really ought to lean on BLS to produce wage and import/export price _indexes_. Disaggregated unit values are better than nothing, but they are not price indexes. Unit values are vitiated by compositional changes.

Inflation Framework: Agree, but I would like to see the Fed lay out how it arrives at its inflation target? Why is 2% better that 1% or 3%. When should it temporarily engineer/allow more? Should it ever engineer/allow less?

The whack at forward guidance was most welcome as was evidence that he is not a low-interest-rate saboteur. Promising price stability with no not to unemployment is a big mistake, but maybe he was just grandstanding. He ought rather to promise the lowest rate of inflation consistent with maintaining full employment of resources. That is more consistent with the Fed's mandate from Congress.