The Costly Rise of Sports Betting

The meteoric rise in sports betting in the US comes at a cost – people are poorer.

Thank you for reading our work! Nominal News is an email newsletter ready by over 1,000 readers that focuses on the application of economic research on current issues. Subscribe for free to stay-up-to-date with Nominal News directly in your inbox:

Our goal for 2025 is to hit 3,000 subscribers:

If you would like to support us further with reaching our subscriber goal, please consider sharing and liking this article!

Since 2018, sports betting in the US has become legal after the US Supreme Court overturned a federal ban. Sports betting in the US grew extremely quickly – by 2023, Americans placed over $120bln in bets, which generated close to $12bln of revenues (this revenue number is net of payouts) for sports betting companies.

As with all forms of gambling, the concern with sports betting is how it impacts the financial well-being of people participating in it. Thus, economists asked the question – did the legalization of sports betting adversely impact people’s finances.

Gambling and Vices

Gambling can be viewed as a form of consumption entertainment given the fact that most participants lose money. In this sense, gambling losses are a cost paid to partake in the entertainment derived from gambling. Since sports betting is a form of gambling entertainment, it can be viewed as part of the spending a person allocates to gambling activities like playing the lottery or casino games. Thus, the legalization of sports betting could have no negative impact on a person’s finances if that person bets more on sports, but then spends less on lottery tickets or other forms of entertainment.

If, however, individuals allocate other money – such as savings – to sports betting, then there may be a risk to their financial situation. Baker, Balthrop, Johnson, Kotter and Pisciotta (2024) (“BBJKP”) set out to determine exactly how the legalization of sports betting impacted finances.

Sports Betting – the Data

BBJKP looked at financial transaction data from 230,000 US households (from an original data set of 60mln households). BBJKP are able to see the income a household earns, as well as the spending on sports betting, along with how much money is being transferred to ‘classic’ investment brokerages (such as Vanguard, Fidelity, etc.),‘gamified’ brokerages (such as Robinhood) and cryptocurrency platforms.

Moreover, for some of the households, BBJKP are also able to see credit card and other loan balances from a separate data set. This is important, as it allows us to see if households tap into additional debt when sports betting is legalized.

Overall, BBJKP find that nearly 8% of households in their sample participate in sports betting. Interestingly, sports bettors are more than twice as likely than non-bettors to have used a cryptocurrency brokerage or overdrawn their bank account. Moreover, sports bettors are also 4 times more likely to have played online poker.

In terms of sports betting, the average amount transferred for sports gambling is about $100 per quarter. However, the top third of bettors contribute nearly $300 per quarter (almost 2% of their income), while the bottom third of bettors deposit only $1.39 per quarter. This suggests that about 2-3% of the households in the sample are betting significant amounts of money. BBJKP also note that if you split the data set in half – into low and high saving households – low savings households that participate in sports betting allocate a larger share of their income to betting and are also more likely to overdraw on their bank accounts.

Betting Trends

To determine the impact of legalized sports betting, BBJKP used the fact that US states legalized betting at different points in time. Thus, it is possible to compare the effect of legalizing sports betting by comparing households in states where sports betting was legalized vs states where sports was not yet legalized.

BBJKP find that after sports betting is legalized, the probability of becoming a sports bettor is 14%. Moreover, after legalization, households that actually bet, contribute around $179 per quarter to sports betting (the overall average, which includes non-bettors, is $25 per quarter). Interestingly, BBJKP also find that the amount contributed per quarter steadily grows after legalization. The amounts start off low – at around $4 to $5 per quarter – but grows to $73 per quarter (both amounts are averages that include non-bettors as well) after 4 years.

This trend in increasing deposit amounts can be, in part, driven by the fact that sports betting companies offer ‘free betting money’ to encourage new sign-ups. However, the increasing tendency in deposits appears to suggest that bettors have a minimum betting amount in mind when sports betting (initially the amount is met by the free sign-up bets, but after that, the bettor has to contribute their own money).

Saving or Consumption

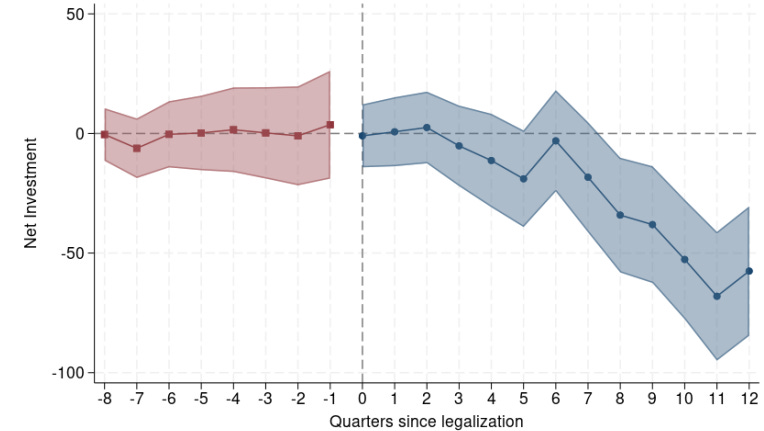

Where does the money for sports betting come from – does it substitute for investment/savings or for other forms of consumption such as entertainment? BBJKP find that after the legalization of sports betting, net investment (deposits minus withdrawals) in brokerages starts to fall. On average, the amount of investment falls by $53 per quarter. The trend is, however, increasing over time, as in the chart below (sports betting is legalized at quarter zero):

More specifically, a $1 increase in sports betting, reduces net investment by $0.99 – so nearly perfect substitution. For low saving households, a $1 increase in sports betting reduces net investment by $3 (this additional drop in savings can be driven by the fact that bettors increase other entertainment expenditures such as watching the games).

Now, it is worth noting that not all investments are the same – investing can also be a form of ‘betting’ if the investments are high risk such as speculative stocks or options (which often have negative expected value similar to betting). Thus, the fall in investments might simply be more ‘sports betting’ but less ‘stock gambling’. BBJKP looked at investments made via more ‘gamified’ brokerages, like Robinhood, and found that, although investments in these brokerages also fall, the size of the fall compared to ‘traditional’ brokerages is 10 times smaller. This tells us that most of the sports betting funding comes from long term investments.

Lastly, BBJKP studied the impact of legalized betting on credit card balances (note – the data for this analysis was limited) and found that credit card balances for low savings households increase, and repayment of credit card bills falls.

Overall, BBJKP find that the legalization of sports betting increases gambling at the expense of savings in traditional brokerages rather than other forms of consumption, and the effect is more pronounced for households that already have a tougher financial situation.

Demand for Gambling

The impact of sports betting shows that there is demand for this form of gambling. BBJKP actually also found that sport betting legalization appears to have increased participation in lotteries. Interestingly, spending on online poker does not increase, suggesting that not all gambling activities are treated the same.

Researchers have also studied if high-risk stock trading can also be seen as a form of gambling. It turns out that there is some evidence for this hypothesis. Dorn, Dorn and Sengmuelle (2015) found that both in the US and Germany, trading in the stock market appears to drop in a week during which lotteries have large jackpots. Moreover, in Germany, there is also a drop in options trading when lottery jackpots are high (options trading generates much greater losses and gains than normal stock trading, so options can be seen as similar to playing the lottery).

Kormanyos, Hanspal and Hackethal (2023) (“KHH”) further investigated the link between gambling activity and stock trading. KHH, using German data, found that people that gamble do not necessarily invest in more speculative stocks (stocks that have a much higher risk) compared to active traders (individuals that buy and sell stocks rather than invest in a stock market index). However, on average, gambling individuals do buy and sell stocks more often by 7% which results in investment returns being about 1% lower than the portfolio returns of non-gambling individuals.

Alternatives to Gambling

In their research, KHH also looked at whether gambling individuals focus on particular sports events, which would suggest that gambling individuals focus their gambling on sports they may possess significant knowledge about. KHH found that in Germany, it appears that gambling individuals do not focus on particular sports but rather their choice of what to gamble on is random. This suggests that gambling is a form of entertainment/consumption for gambling individuals.

Combining this research with the findings of BBJKP (that gambling individuals fund gambling by reducing their investments), new ideas have been proposed that merge the entertainment value of gambling, while also protecting investments. In 2009, Michigan rolled out the first large scale Prize-linked savings account (PLSA). These PLSAs merge savings accounts with a random chance of a reward. That is, rather than earning a guaranteed rate of return like a typical interest on a savings account, a bank will pay out the interest payments as a prize with some probability of winning.

Cookson (2017) found that PLSAs rolled out in Nebraska in 2012 resulted in a 4% to 10% reduction in the amount spent on gambling. Moreover, the likelihood of visiting casinos fell by 15 percentage points in counties that had at least one institution offering PLSAs. Deposits into savings also increased as the raffle date for the PLSA prize drew closer (note – each dollar deposited into a PLSA increases the likelihood of winning the raffle for the prize). Cookson thus found that PLSAs did confer some of the entertainment value of gambling, while also protecting people’s investments.

The Complexity of Gambling

As the research above shows, gambling is a complex issue. With the growth of ‘gamified’ brokerages, even the definition of gambling itself is no longer clear. Gambling does appear to be a form of entertainment that occasionally can be very costly, as with any vice. When governments choose to make access to gambling simpler, whether via legalization of sport betting or brokerage gamification, it can come with significant costs. At the same time, governments can offer or encourage solutions that enable individuals to get the entertainment value of gambling, while also protecting people’s finances.

Interesting Reads from the Week

Article: Riccardo Vocca discusses how consumers prefer gadgets to be ‘smart’ when their scope of usage is wide (smart phone), but prefer their gadgets to be ‘simple’ when the usage is narrow (smart locks).

Article: Alpha in Academia covers how professional basketball teams in the NBA and baseball teams in the MLB perform worse after having played a game in a ‘party-city’ such as New York or Los Angeles.

US Labor Market Update: As always, Pascal Michaillat updates us with key macro labor indicators (recession probability went down), and Guy Berger gives us the labor figures (unemployment fell last month).

Social Media Posts from Nominal News

Below are some topics we discussed this week:

On Congestion Pricing:

On CEO pay solutions:

The US Department of Justice recently sued users of the rental pricing algorithm for collusion:

If you enjoyed this article, you may also enjoy the following ones from Nominal News:

Community Civilian Interventions (June 12, 2023) – cities have always been interested in improving safety in neighborhoods. Civilian government interventions have been proposed as a solution instead of police. However, civilian interventions work best if local government presence is strong.

Higher Education – Is It Worth It? (December 10, 2024) – do the extra years of schooling at college increase peoples’ skills or is college just an expensive signal? A recent study suggests it’s the former.

Economic Brain Teasers (August 20, 2024) – economic brain teasers can be helpful to clarify ideas, but it is important to be clear about the assumptions being made. Using them for ‘gotcha’ style questions is counterproductive.

I really enjoyed this post. The net investment figure is powerful

Thank you a lot for the mention, and I really liked this issue!