Impacts of Student Debt

The US Supreme Court is hearing the case regarding the partial student debt forgiveness. What are the costs of funding college education via debt?

Summary

Student debt is a unique issue to the US, especially given its magnitude, which has grown in recent years.

College funding is done in the US using student debt, while in many other countries, the costs are paid by taxpayers.

There are both direct and indirect effects of student debt to the whole economy, which may influence the calculation of which system is better from a taxpayer perspective.

Student debt reduces future pursuit of further advanced degrees and reduces employment in socially beneficial jobs.

The impact of student debt on earnings and homeownership is ambiguous, as it depends on the group that is impacted.

In the US, there are improvements, such as income based repayment schemes, to the current system that can be made that will lead to better outcomes for both students and taxpayers.

Introduction

On February 27 and 28, 2023, the US Supreme Court heard the case involving President Joe Biden’s partial student loan forgiveness. The outcome of this hearing is not expected until June and rests primarily on a variety of legal interpretations – one key point of contention is whether the plaintiffs (the states that challenged Biden’s student loan forgiveness program) are actually harmed by the forgiveness. We’ve previously discussed whether this student loan forgiveness will be beneficial to the US economy, and found that it would probably be beneficial to the US economy and taxpayers. As mentioned in my prior article, this time around we’ll look at what are the different impacts of funding college via taking out student debt.

Student Debt in Perspective

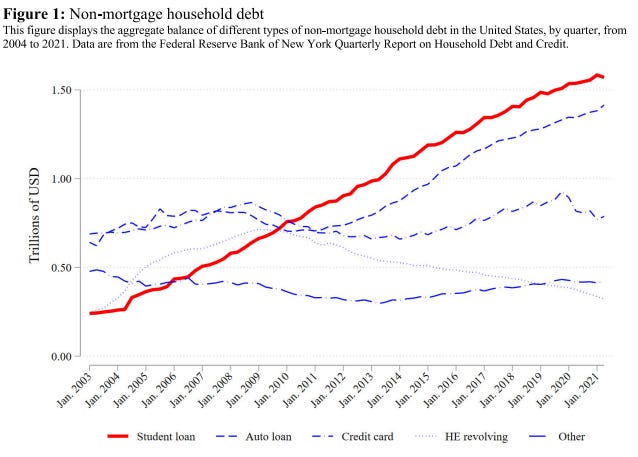

Student debt is a problem that is relatively unique to the US. Many other countries offer free college education to their citizens, meaning that taking out debt is not necessary to fund higher education. To quantify the issue of student debt, approximately 30 to 40 percent of undergraduate students take out student loans per year, and 70 percent of students that receive a bachelor’s degree carry some amount of student debt after graduation. The average federal student debt balance is around $37,500, with private loan balances reaching an average of $55,000. To put these amounts into context, the average pre-tax pay for a college graduate is around $55,000. Overall, 45.3 million people currently have student loan debt. Student loan balances remain high for a long time after graduation – 20 years after entering school, half of student borrowers still owe more than $20,000. One of the reasons for these high balances is the fact that interest rates on student loans are not very low – student loans disbursed in 2018 had a 5.1% interest rate (the Federal Reserve interest rate was between 1.50% to 2.50% during that time). Federal student loans are also capped at how much one can borrow - in 2018/19 the cap was at $31,000. Thus any shortfall in funding would need to be covered by other financial sources – if it’s not parental income, it would be either private student loans or federal parental loans. However, these loans come with higher interest rates - parental loans in 2018/19 had an interest rate of 7.6%. Student debt in the US represents quite a large share of total debt – total US loan debt stands at $1.7trln, while total non-housing debt (not mortgages) is around $4.5trln. Below is the historical trend in student debt (Yannelis and Tracey, 2022).

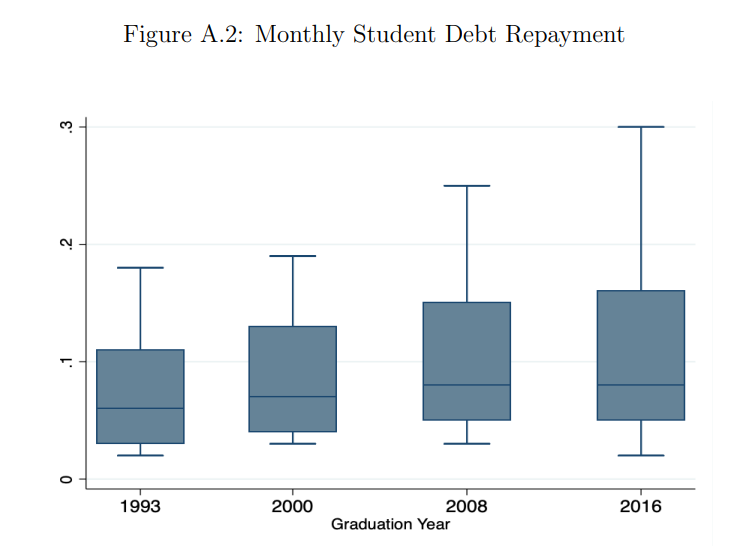

Student loan repayments as a fraction of monthly income have also gone up over time. In the box-plot graph below, the y axis represents the percent (decimal notation) of monthly income needed to pay the minimum monthly payment for student loans. The middle line in the box is the average percent of income, while the top and bottom of the box are the 75th percentile and 25th percentile. The ‘whiskers’, the farthest lines out, represent the maximum and minimum.

The current system in the US places a significant part of the cost of higher education on the individual and their family. In other countries, where college education is funded by the government, the cost is ‘socialized’, meaning all taxpayers bear part of the burden. Obviously, college students benefit from the socialized system because their cost is much lower while they gain the same, or nearly the same benefit (there is a discussion on whether allowing colleges to set their own prices for tuition results in the provision of better education). One might assume, therefore, that the current US system results in an overall better outcome for the taxpayers by saving them money. However, student debt may have many indirect effects that have wide-ranging impacts on the whole economy, resulting in indirect costs to the taxpayers. The question therefore is, do taxpayers benefit more from the socialized higher education system in comparison to an individual student debt system. Below, we look at some of these costs that will help inform the debate on which system is preferable for taxpayers.

Student Debt Impacts

So why should student debt be different from other forms of debt such as auto-loans, credit card debt or mortgages? The key difference between student debt and nearly all other forms is its timing – student debt impacts people who typically have no income, no wealth, and no credit history. All other forms of debt rely on the aforementioned factors and are only issued to people that will be able to repay it over time. Furthermore, other forms of debt such as auto-loans and mortgages are backed by a physical asset. In instances when repayment becomes difficult, the debt issuer can get the physical assets to pay off the debt. With student, there are no assets backing it. Moreover, student debt is unique to other debts as it is not dischargeable in bankruptcy. Bankruptcy, which is a procedure intended to allow individuals or businesses to free themselves from debt, does not apply to student debts, which means, saying crudely, you are stuck with it.

Knowing that student debt is a burden that will not only grow due to the high interest accumulation, but is also not dischargeable, will likely impact decisions made by students after graduation. To study these impacts, economists have mainly focused on using ‘natural experiments’.1 One crucial impact of student debt is the choice by bachelor degree holders to pursue further education and enroll into graduate school. Chakrabarti et al. (2022), utilizing the fact that certain universities significantly changed tuition, found that a $5,000 increase in undergraduate tuition reduces graduate school enrollment by 3.1 percentage points and increases student debt by $1,480. The long-run impact of this decision on society has not been established, but discouraging students from pursuing advanced degrees could potentially adversely impact our knowledge frontier. Furthermore, human capital (i.e. the overall level of knowledge and skills) of an individual represents a significant component of that individual’s wealth (Palacios, 2015). Human capital acts as a buffer to negative shocks in the economy, as it enables the individual to continue spending during bad times. For example, if the individual’s returns to capital (e.g. rental income, stocks) fall in bad times, your total income would be lower, and a larger share of that income would be related to your work related earnings, which are based on human capital. Thus, the overall level of human capital, potentially reduced by student debt, acts as a natural stabilizing factor in the economy.

Addressing a slightly different question, Rothstein and Rouse (2011), using the fact that certain colleges switched to ‘no-loan’ policies (when determining financial assistance, colleges do not assume students will take out loans), found that student debt results in students not taking public interest jobs after graduating as often. Field (2009) found a similar result using a financial aid experiment at New York University. In her study, students were given one of two financially equal aid packages – either a loan that would be paid off by the school as long as the student worked in public interest law for 10 years, or fully paid the tuition as long as the student worked in public law (also for 10 years). If the student did not, they would have to reimburse the school. Although both options are financially identical, students that received the tuition subsidy were 36 to 45 percent more likely to enter public interest law. Just the psychological impact of debt altered the decision, pushing students towards higher paying private sector jobs. This effect on lawyers was also shown by Sieg and Wang (2018). A similar trend was also found in the field of medicine, with higher debt loads reducing the likelihood of becoming a primary care physician (Rosenblatt and Andrilla, 2005), instead preferring to become a specialist where pay is higher, but the public need is lower. In addition to different career choices, Sieg and Wang also found that women with more student debt stay longer in private sector jobs, postpone marriage, marry men with lower earnings, and delay childbearing.

Student debt has also been shown to reduce entrepreneurship (Krishnan and Wang 2018, Chemmanur et al. 2023). This is due to the fact that student debt exacerbates the effects of negative business outcomes, discouraging debt holders from starting a business in the first place. Student debt may also impact homeownership – Mezza et al. (2020) found that an additional $1,000 in student debt reduces homeownership by 1.8 percentage points, potentially partially explaining the reduction in homeownership among 24-32 year olds (from 45% to 36% between 2005 and 2014). Not all studies confirm this finding on homeownership. Folch and Mazzone (2022) argue that student debt impacts the choice of an individual on whether to pursue further education or purchase a home (i.e. increase current consumption). A person with student debt is less likely to choose further education, because it delays their consumption and homeownership, as their contemporaneous net wealth is more likely to be negative and further education only pays off in the medium to long term. Folch and Mazzone found that “an increase in student debt by 10% at graduation leads to a decrease of 6 percentage points in the likelihood of holding a graduate degree and a decrease in annual earnings of 3.2% ten years after graduation.” They find that homeownership rates, on the other hand, aren’t impacted negatively by student debt.

All of the above effects impact the wider economy and, indirectly, taxpayers. Having skilled individuals not take public interest jobs impacts us negatively, while postponing household formation impacts long run demographics. These are real costs to taxpayers, which have not yet been evaluated in a context of a general equilibrium model.2

Student Debt and Earnings

The indirect impact that is easiest to quantify is the impact of student debt on earnings. If student debt impacts earnings, it would also impact tax revenues and returns to the taxpayer.

One of the more important impacts of student debt is how it impacts earnings. There are several possible channels student debt this can influence earnings: 1) possessing student debt will encourage students to seek out higher paying jobs due to the burden of the debt; 2) student debt can induce people to work more hours; 3) student debt can reduce earnings by reducing future educational attainment; and 4) student debt can result in worse job searches, leading to an inferior job matches with lower earnings.

In general, economics research has found evidence to support each of the above channels, depending on the group studied and data used. For example, as mentioned above, lawyers and doctors choose higher paying jobs at the expense of public interest positions. However, Folch and Mazzone (2022) and Chakrabarti et al. (2022) found that earnings go down for student debt holders that would have potentially pursued further advanced degrees. These two examples illustrate how both statements – that student debt increases earnings and decreases earnings – can be true at the same time. For advanced degree holders such as lawyers and doctors, student debt causes them to take on higher paying jobs, while for undergraduates finishing college, student debt causes them to not pursue these advanced degrees.

Student debt has been shown in some instances to induce the debt holder to work longer hours rather than earn more per hour (Daniels and Smythe, 2020). These lower hourly earnings may be partially explained by the fact that student debt holders do not undertake as much on-the-job search for new opportunities, fearing getting laid off from their current position (Ji, 2021). Also, students are less likely to migrate to other locations to look for higher paying jobs, believing that staying locally with their family will save more money to pay off the debt (Di Maggio, Kalda, Yao, 2020). In studies where overall earnings are higher for student debt holders, one offsetting factor is the non-pecuniary (i.e. not monetary or financial) job benefits. Luo and Mongey (2019) found that higher debt burdens push graduates to take on higher paying jobs with lower job satisfaction (high satisfaction jobs have a value equivalent to 6% of lifetime income).

Conclusion

The US financing of higher education is unique. Whether it is a macroeconomically beneficial system in its current state hasn’t been studied holistically, as it involves a lot of different economic interactions (and we haven’t analyzed the impact of high college costs on the decision to go to college and which major to earn a degree in). However, the above analysis has shown that there are definitely problems in the current higher education system that can be addressed, leading to improvements for the whole economy.

A lot of these problems are caused by how the US undertakes the process of funding colleges. There is a crucial incentive misalignment between the student, the college, and the government. Since a majority of the student loans are guaranteed by the government, colleges are not concerned whether students will be able to repay these loans in the future. In cases the students aren’t able to repay the debt due to poor labor outcomes or bad luck, the taxpayers end up footing the cost of the education. This results in situations where colleges sign up students that are funded by government backed loans, knowing that they will be paid, which also allows them to charge higher tuition. This is a situation where the financing of the payments (the federally backed student loans) and the recipient of these payments (the college) would be better off treated as one unit rather than two separate entities. As one unit, the incentive issue disappears – either via controlling who receives the funding (for example incentivizing certain majors) or via controlling the tuition and encouraging cost efficiencies at the college. Having financing separate from setting the price of education (tuition) leads to a breakdown in the incentive alignment resulting in a high student debt world with worsening outcomes.

Solving the above issue would require a significant overhaul of the current setup in the approach to higher education. However, in the meantime there are a lot of targeted solutions within the current system that would yield benefits. The Income Based Repayment programs alleviate some of the concerns established above. Student debt holders do not have to worry about repaying debt and can for example seek out other job opportunities. The idea of offering student loan forgiveness for students that take up public interest jobs also appears to be a net positive for the economy, especially when enacted as a tuition subsidy. Discharging in bankruptcy should also be re-evaluated. Studies have shown that student debt holders who are in default, end up improving the economy once their debt is forgiven. Yannelis and Tracey (2020) argue that although there could be strategic filing for bankruptcies (i.e. a student would ‘game the system’ by filing for bankruptcy right after graduating to discharge the student debt and then accumulate assets), that impact is far lower than the welfare benefits generated by bringing back bankruptcy to student loan debt.

In the hard-sciences (e.g. biology, chemistry), an experiment is when we take two groups and treat one of them with an intervention (for example, a medicine) and argue that any difference of outcomes between the groups is due to the treatment. That is because there shouldn’t be any difference in the group prior to the treatment if the enrollment into the groups was random. In social sciences (e.g. economics, psychology), such experiments are usually not allowed for ethical reasons or not feasible. However, they tend to occur naturally due to laws and regulations that arbitrarily divide people into two groups. For example, two groups with no discernible difference between them: one that receives government intervention and one that doesn’t.

A general equilibrium model attempts to look at the impacts of policy or decisions on the whole economy, including any direct and indirect effects. Partial equilibrium models focus mainly on certain parts of the economy or subsets of individuals. Many empirical studies (including the ones cited here) inform us about the partial equilibrium as we get specific information about one particular impact on a narrow group of individuals.

What a great article! Very informative!