The Changing World of Competition

The recent cases of employee 'no-poaching' lists and the use of algorithms for rent pricing, highlight how maintaining competition has become challenging.

Thank you for reading our work! Nominal News is an email newsletter read by over 1,000 readers that focuses on the application of economic research on current issues. Subscribe for free to stay-up-to-date with Nominal News directly in your inbox:

Our goal for 2025 is to hit 3,000 subscribers:

If you would like to support us with reaching our subscriber goal, please consider sharing and liking this article!

Competition and anti-competitive practices continue to be a hot button topic. Recently, a merger of two large grocery chains in the US was blocked. A US airline merger was blocked in March 2024 (with one of the airlines filing for bankruptcy shortly afterwards). Competition has also been referenced in the context of the 2021-2022 inflationary surge, with limited competition among firms potentially amplifying inflation.

The changing economic landscape, with both globalization creating mega-corporations and new digital technologies allowing for unprecedented data usage, has not only resulted in new research, but also a debate on the correct level of antitrust enforcement. Economic research has illuminated how some of these new developments have impacted our understanding of anti-competitive behavior, informing our discussion on antitrust enforcement.

Collusion – Common Leadership

Collusion is a secret agreement between firms to limit competition. Firms will typically collude over a variety of issues such as agreeing to not undercut each other’s prices or agreeing to not poach each other’s employees.

One way collusion could occur if firms share common leadership, i.e. the firms’ share an executive or a board of directors member. The concern is that a person with such an influential position in both firms can directly get the two firms to collude. The US actually has a specific law – Section 8 of the Clayton Act – that prevents such common leadership under highly specific situations, which may be difficult to prove.

At the same time, prohibiting executives from working in two companies can also have an adverse impact on the economy. It potentially reduces the knowledge spillover between firms, as well as artificially prohibits firms from tapping into a pool of executives. Thus, a blanket ban may be harmful, and it is important to determine if collusion under common leadership does occur.

Silicon Valley – “No Poaching” Collusion

In the 2000s, several high-tech companies, including Apple and Google, were accused of colluding by agreeing to not recruit each other’s employees. This resulted in a lawsuit filed by the US Department of Justice, which ultimately resulted in a settlement. After the settlement, the evidence from the lawsuits was unsealed, which allowed us to see which companies were most likely colluding amongst themselves.

Herrera-Caicedo, Jeffers and Prager (2024) (“HJP”) used this data to estimate the impact of common leadership on the probability of collusion. The dataset constructed by HJP showed that there were 45 colluding firms, with each firm having on average 2 to 3 collusion agreements. To illustrate the collusion issue, HJP give the following example:

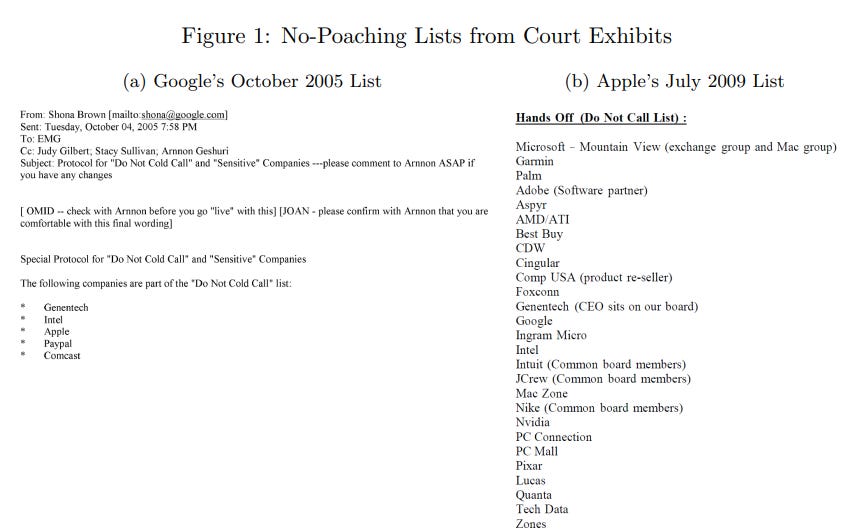

“For instance, in 2005, Arthur Levinson served as CEO of Genentech and board director for Apple and Google. We consider Genentech, Apple, and Google connected through common leadership at that time. Genentech, Apple, and Google all entered into no-poaching agreements with each other.”

Below is an image of how such no-poaching agreements looked like:

Based on the unsealed evidence, 62% of the firms that had been colluding had a common leader with at least one other company in the lawsuit over the 2000-2009 period. Moreover, if we look at the data more granularly, the common leadership issue becomes even more salient. If a pair of companies never shared a leader, then the probability of them having colluded was 5%. If a pair of companies did share a leader, that probability rose to 35%.

On its own, these statistics are startling. But the economic question HJP are attempting to answer is what is the impact of common leadership on collusion probability. It is worth noting that two firms may have already planned to collude and the hiring of each other’s leaders may be a way to facilitate this collusion. HJP, although cannot entirely dismiss this pattern, finds evidence suggesting it is unlikely. For example, collusion is not implemented faster after the common leader is hired. Moreover, the emails from the unsealed documents suggest that the reason for collusion in certain instances was the common leader.

Assuming the hypothesis that common leadership causes collusion, HJP found that the probability of collusion went up 11-12 percentage points after the appointment of a common leader. This jump in collusion is large, as the average probability of collusion is 1%-2% in the sample.

Moreover, although the lawsuit focused on high-tech companies, it is important to note that the issue of common leadership occurs often in the wider US market. HJP states that 38% of public firms share a common leader with one other firm, with 14% of public firms sharing a leader with at least one other firm in the same state. Thus, there is potential for significantly more anti-competitive behavior that may need to be analyzed.

It is worth noting that such collusion against workers may have costs beyond just the directly impacted workers in the high-tech sector. Wages and salaries of jobs in one industry can serve as reference points when workers in other firms/industries negotiate their wages. Thus, if high-tech workers get paid less, this may impact wages of other workers, say in finance, which may then impact wages in another sector and so on. Collusion in one sector can have impacts on other industries.

Housing Collusion

The above example focuses on collusion that hurts workers. More traditional collusion hurts consumers. One recent high profile case of collusion occurred in the real estate market with the use of software by a company called RealPage. RealPage’s algorithm, named YieldStar, provides owners of multi-family homes a price to charge for each rental unit. An algorithm, such as YieldStar, can impact the wider rental market both positively or negatively.

Positive Impact – “Responsive Channel”: an algorithm can make rent prices adjust more rapidly to market conditions, improving overall market efficiency and welfare.

Negative Impact – “Coordination Channel”: an algorithm, intentionally or unintentionally, can lead to market collusion.

Calder-Wang and Kim (2024) set out to test which of the two channels was larger under the RealPage algorithm. Under the Responsive Channel, the market is more competitive as the algorithm aims to maximize the profit of each landlord separately. Thus, under the Responsive Channel, an algorithm user will reduce rental prices quicker than a non-algorithm user during economic recessions, in order to maximize occupancy. This, for example, occurred during the Great Recession in 2008 (the same style software was available then). During an economic boom, the algorithm-user will increase rental prices faster than a non-algorithm user since potential renters are willing to pay more.

Under the Coordination Channel, the algorithm will focus on maximizing profits jointly of all landlords that use the algorithm, rather than of each particular landlord. In this instance, the algorithm ‘knows’ that by recommending a lower rental price for one algorithm-user, the rental prices of all other algorithm-users will be impacted as well. Thus, if the algorithm is more focused on the Coordination Channel, the algorithm will always recommend slightly higher rental prices (akin to a monopoly firm)1 than if the algorithm was purely operating under the Responsive Channel.

To determine whether the Responsive or Collusion channel dominates, it may be tempting to simply compare the rental prices of algorithm users to non-algorithm users, and see if algorithm-users charge higher rental prices than non-algorithm users suggesting Coordination. However, this would be incorrect. As described above, under a Responsive Channel, algorithm-users will charge higher rental prices than non-algorithm users during economic booms, because algorithm-users respond faster to new economic developments. The use of the algorithm would still be optimal from a society perspective.

Thus, Calder-Wang and Kim built a model of rental price setting. Using the model, along with data on rental prices and knowing which buildings set prices using the algorithm, Calder-Wang and Kim could test whether the Responsive Channel dominates the Collusion Channel or vice versa.

Calder-Wang and Kim found that the Collusion Channel appears to dominate. The net impact of algorithms appears to have increased rental prices by about $25 per month per unit. Since the total number of housing units that use algorithm pricing is estimated to be 4.2mln, the total impact of algorithms appears to be nearly $1.3bln per year. This is also likely to be the lower bound estimate, since it does not include the spill-over effect – that is, the higher prices of algorithm-user priced rental also push rental prices of non-algorithm user rentals. The problem might become bigger, since in 2017, RealPage acquired a competitor rental pricing algorithm, Lease Rent Option, effectively controlling 95% of all algorithm-users.

It is worth noting that conceptually, such an algorithm could still be a good tool. Since Calder-Wang and Kim did not have access to the algorithm and its code, it is unclear why the YieldStar algorithm resulted in increased rental prices. In part, the lawsuit filed against RealPage could help illuminate whether the higher rental prices are a natural consequence of algorithm pricing or whether this collusion was intentionally built-in. The latter can be fixed with the usage of open source software.

Changing World – Changing Antitrust

Antitrust is a very complex area of economics. Determining what is the right amount of antitrust enforcement and what constitutes unfair competition is not easy. Technological change, like algorithms, can both increase and decrease competition, and establishing which will happen is nearly impossible. The growing occurrence of common leadership can also be both bad and good, as it increases knowledge sharing, but also increases the likelihood of collusive behavior.

Too aggressive antitrust can adversely impact innovations and knowledge-sharing. Too lax antitrust can have very high societal costs. With rapid technological change and globalization, many approaches to determining whether something is pro- or anti-competitive can become outdated very quickly. The debate around antitrust, however, is often not framed as a discussion on how to ensure positive outcomes to society, but rather as a partisan issue. Instead of focusing on how to effectively incorporate academic research and data to respond quickly to anti-competitive outcomes, too often the focus is on manipulating data and analysis to push a point of view (and economists are guilty of this too, especially in front of judges).

Interesting Reads from the Week

News: Congestion pricing is set to start on January 5 in New York City – the first city in the US to implement such a system. We will monitor the outcomes from this new program.

Article: Yaw discusses the historical patterns of Intellectual Property diffusion (or theft) between countries, as well as safe-guarding Intellectual Property.

Article: Guy Berger presents his 2025 US labor market outlook. It can be summarized as follows: “The most likely labor market outcome for 2024 is an end to the labor market cooling process we’ve experienced over the past 2.5 years.”

If you enjoyed this article, you may also enjoy the following ones from Nominal News:

Monopolies and Antitrust Enforcement (November 20, 2023) – with news of the Federal Trade Commission suing Amazon for anti-competitive practices, economic research suggests that such lawsuits typically improve overall welfare.

Tariffs, Tariffs… (Electoral Issue Series – November 4, 2024) – tariffs are a bad economic tool. However, there may be one scenario in which they can work – correcting global and domestic carbon emissions.

To Compete or Non-Compete (April 30, 2023) – why non-compete clauses do not solve any issues, but only create costs.

Under perfect competition, the price of a good or service equals the marginal cost. That is because if a firm sets a higher price than the cost to produce, another firm will undercut this price. This means no profits are made since the price received for a good equals the cost to produce it. A monopoly (or colluding firms) would set a price slightly higher to maximize profits.

We lose healthy competition daily. Fubo TV just bent the knee to Disney, so now we’ll get more Hulu with ads shoved down our throat. We need more disruptors not less.