Trump's Childhood Savings Accounts – A Flawed Policy

Why these new savings accounts for children are neither likely to help low-income families nor materially increase savings.

Nominal News is an economics newsletter written by a PhD Economist that translates the latest economic research into clear, policy‑relevant insights on current issues. Join 4,000 readers for free to stay-up-to-date with Nominal News directly in your inbox:

Financial well-being, especially of children, is an issue that many countries grapple with. US President, Donald Trump, announced a policy in which newborns born between 2025 to 2028 will receive an investment account with $1,000 in it provided by the US Treasury (i.e. US tax payers). The money in the “Trump Account” can be invested in certain stock market funds, but the funds themselves can only be accessed after the child turns 18.1

Now, on paper, this policy sounds good, as we’re boosting savings for families with children. But, upon closer inspection, this is a policy that does not actually help much at all – and it’s not because the amount of money invested is small. Let’s dive in.

Alleviating Child Poverty

Before we start assessing the Trump Account policy, we should first determine what it is that we want to achieve with the policy. A policy is just a tool to achieve a goal. The goal, at least to me, is to improve outcomes/welfare for children and, perhaps, teach children and families to save/invest via exposure to markets.

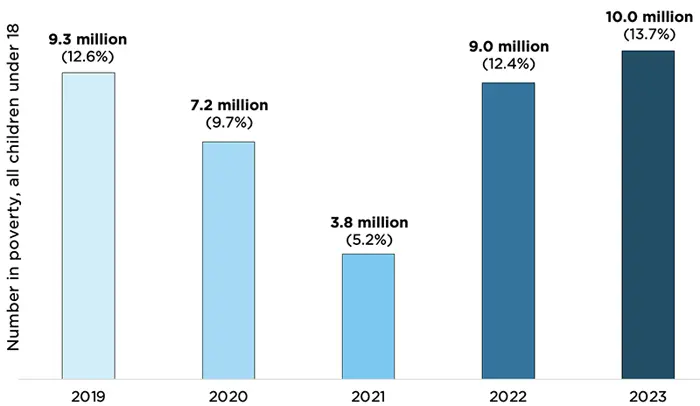

Child poverty in the US is a serious problem. Around 12%-14% of children live in poverty2:

On the above chart, you may notice that, in 2021, there was a dramatic fall in child poverty, which then rebounded to the current highs. The reason child poverty fell in the US was thanks to the numerous government programs helping low income families, of which the 2021 Expanded Child Tax Credit3 (eCTC) was the most important. We’ve discussed this policy extensively here, and argued that it is a policy that pays for itself. The eCTC was a 40 times larger program than “Trump Accounts”, but the reason it worked had to do more with the fact that it immediately alleviated issues for families in need. Per every $100 a family received:

$28 was spent on food;

$31 on housing; and

$15 on child related goods and services.

On the other hand, a savings account will have none of this impact, as the money is locked until age 18.

Some might argue that these families who receive the “Trump Account” could increase consumption by saving less in other accounts. The problem with this argument is that families in poverty do not have savings, and thus they cannot ‘tap’ into other savings.

Therefore, for low income families, this policy will not have any meaningful impact, at least for 18 years.

Shuffling Savings

Turning to non-low income families who already may have their basic needs met, “Trump Accounts” could in theory benefit them by increasing and encouraging more saving. However, as these families may already have savings, it is unclear whether their overall savings will increase by the full $1,000 amount. That’s because a family may choose to save less in other accounts (savings accounts, personal brokerages, etc).

Research on other types of tax-advantaged accounts (i.e. saving accounts that have certain tax benefits) have shown that adjusting savings is common. Benjamin (2003) showed that when a person becomes eligible to use a new tax-advantaged retirement saving account, only around half of the funds that are put into the new tax-advantaged account are truly new savings. The rest is simply shuffling savings from a different account. Other studies found even lower percentages – Fehr, Habermann and Kindermann (2008) showed that only 22% of funds in tax-advantaged accounts are truly new savings, while Pence (2001) argued that the percentage may actually be 0%.

Regardless, this tells us that many families will simply adjust their other savings in response to the “Trump Accounts”. Intuitively, it makes sense. Suppose you have a rule of thumb that you save 30% of your income. If you receive an unexpected $1,000 in income, you may end up spending $700 more now to maintain the same ratio of consumption to saving.

Therefore, the “Trump Savings” account will not increase saving by a significant amount. Furthermore, in effect, tax payers will be subsidizing the consumption of higher income families, as the funds in the “Trump Accounts” come from tax payers.

Negative Impact on Recipients

While researching for this piece, one thing that surprised me is that there may be “Trump Account” recipients that can end up worse off. This surprising outcome is driven by how different government programs interact. Dynarski (2003) showed how similar tax advantaged accounts – the 529 savings plan, which allows families to save money tax free to be used to cover children’s college costs – can end up harming users. That’s because the US also gives college applicants financial aid that depends on the financial situation of a family. Thus, if you save enough, you may no longer be eligible for financial aid, resulting in no benefit whatsoever from saving.

Although this may be somewhat of an extreme case, it’s worth noting that not all the accumulated savings in “Trump Accounts” may end up truly staying with the recipient.

Financial Literacy

So is there an aspect where this policy may have larger positive impacts? One way “Trump Accounts” may be helpful is that it exposes people to saving and stock market investing. This in turn could lead to more saving/investing in the future, as children exposed to savings/investments will become adults that are more financially literate.

The question therefore is – does having an account from birth lead to children and their parents becoming more financially literate? The evidence on this is mixed (and the amount of research on this topic is limited). There have been similar programs enacted at the state level in the US – for example, the SEED Oklahoma program, where several thousand children received a $1,000 savings account at birth that was to be used for college. Results were mixed, as several analyses showed positive impacts (more likely to go to college, higher savings), but under closer inspection, a lot of these outcomes were driven by wealthy families.

An Experiment

A potentially better method to improve financial literacy is to actually teach children in school. Horn, Jamison, Karlan and Zinman (2023) (“HJKZ”) undertook a financial literacy experiment in Uganda. HJKZ took 2800 Ugandan youths and split them into 4 groups:

Group 1 was given no intervention;

Group 2 was given access to a savings account at a bank;

Group 3 received financial education; and,

Group 4 got the account and financial education.

The outcomes that were studied included – overall financial literacy, trust in financial institutions and the amount that was saved. One year after the intervention, the two groups that received education showed higher financial literacy and trust in financial institutions, while the group that only got the bank account showed no change.

With regards to saving, a similar pattern occurred – groups receiving financial education had higher savings (Note: since the study had a relatively small number of participants, HJKZ could not conclusively reject that the group that only had the account saved less than the education groups).

HJKZ followed up on this study five years later. Surprisingly, the financial literacy of the two education groups reverted to pre-finance education levels, although trust in institutions remained. Savings behavior remained similar to what happened after one year (higher savings than the group that received no account/no financial education, but unclear whether higher than the group that just received the account).

Overall, with the caveats that this is just one study, it appears that any intervention (whether account opening or education) has some positive impact with increased saving. In general, financial education appears to be slightly better than just having an account. Either way, the cost of either helping youths open bank accounts or provide education is relatively low, and thus it may be beneficial to conduct these interventions either way.

How To Improve the “Trump Account” Idea

I will first note that the “Trump Accounts” program is a small program. With about 3.5mln births in the US per year, the direct cost would be $3.6bln annually (for comparison, the Child Tax Credit program currently costs $128bln).4

However, we should still evaluate the program based on whether this is an effective spend of money. I feel quite comfortable saying “no” – the “Trump Accounts” are a poor spend of money. If the aim is to improve outcomes for low income families, then direct unconditional assistance (such as the Child Tax Credit program) is superior. If the aim is financial education, then a better program could easily be designed at the same cost.

For example, opening savings/investment accounts for school children coupled with a financial literacy course would probably be better. These accounts could also start with a government investment, albeit at a lower amount like $100. Moreover, since financial literacy dissipates, perhaps, refresher courses every 3-4 years would be beneficial. As part of completing these courses, students could get another $100 added to their account. This would encourage participation in these financial literacy classes. Students exposed several times during their studies might come out far better equipped.5 This policy would likely be much more effective and cheaper than the “Trump Accounts”.

Financial literacy and saving is an issue faced by all societies. Although today we focused on the US (and Uganda), I believe these findings are applicable globally.

Let me know your thoughts on these accounts and what you think would improve financial literacy.

If you would like to support us in reaching our subscriber goal of 7,000 subscribers, please consider sharing this article and pressing the like❤️ button at top or bottom of this article!

Interesting Reads from the Week

Stop looking at economic averages! – Troy Tassier discusses why focusing on average statistics does not paint the whole picture of the economy – distributions matter.

Political journalism needs fewer “takes” and more analytical legwork – G. Elliott Morris highlights the current problems with political journalism, which is similar to what we see in economics.

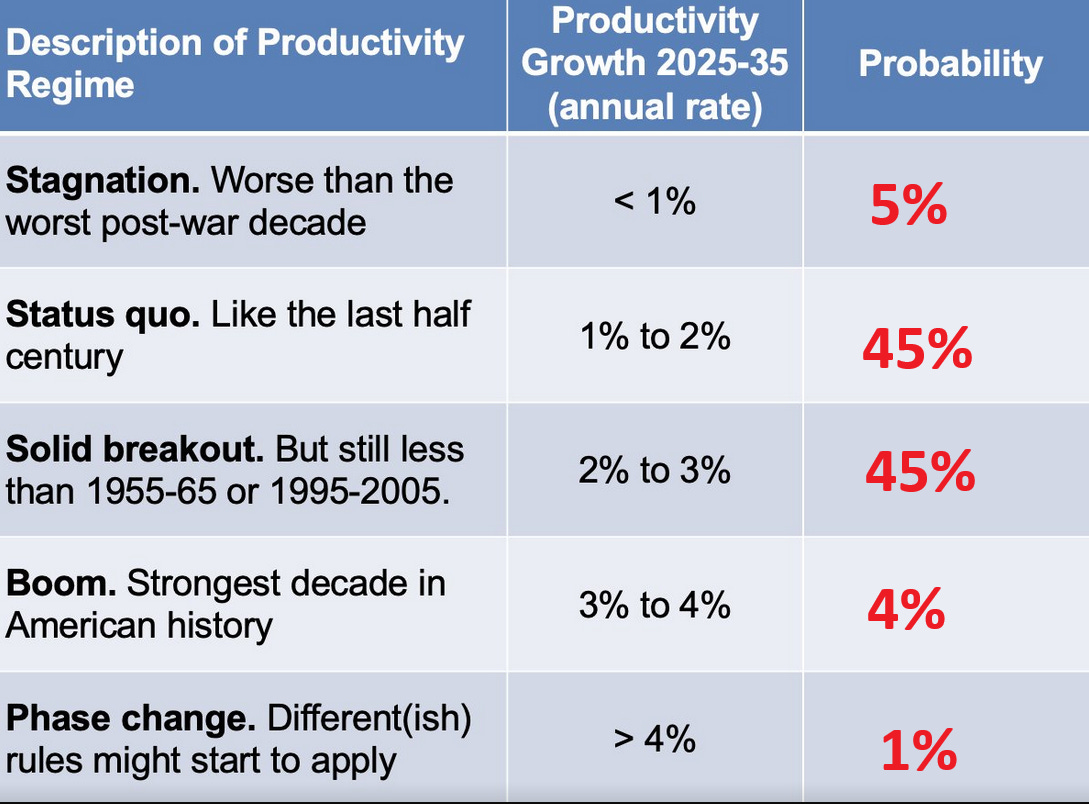

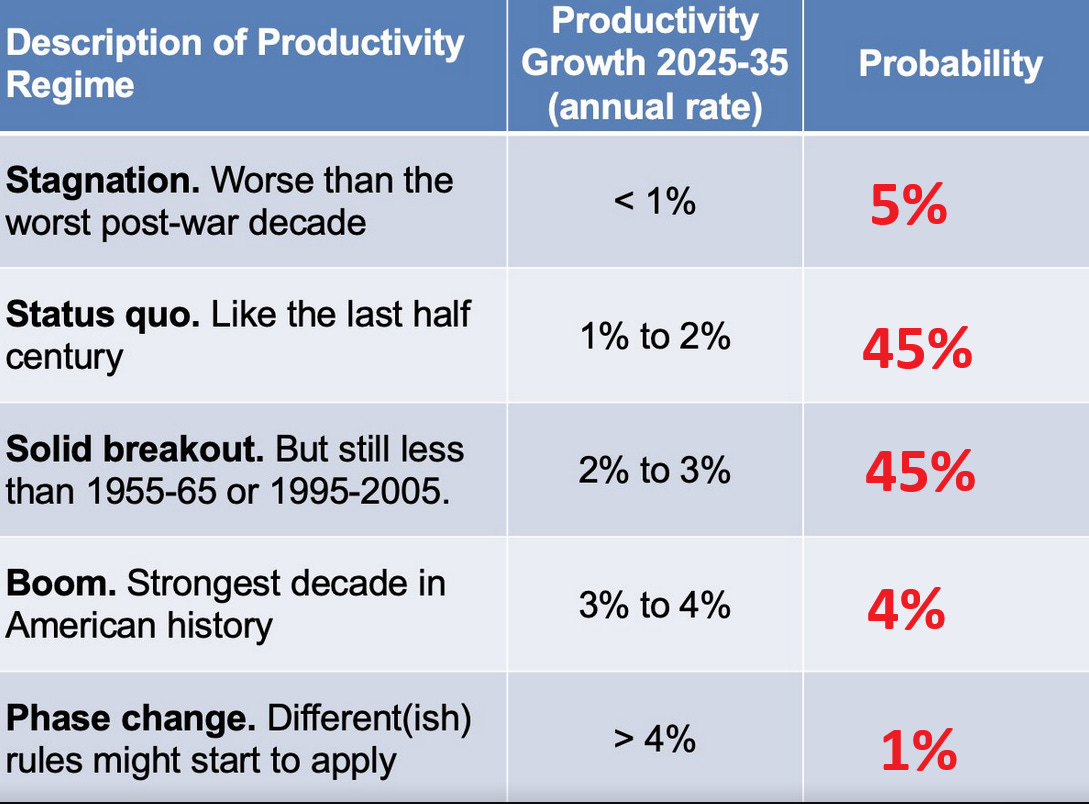

Prediction – Jason Furman asked people what they think average annual productivity growth will be in the next decade, when taking into account AI. He provided a table of 5 possible outcomes, and asked readers for their probabilities. Here is Nominal News’ forecast in red:

Generally, I do not expect any major surprises. I do worry that there might be an ‘accidental’ recession that could happen due to misuse of genAI (similar to the financial crisis of 2008 and the misuse of collateralization calculations). My main reason for forecasting a solid breakout is that energy costs may drop in the next decade allowing for greater production + genAI lowering the cost of trying out new ideas, especially in early phase applied research.

Families and employers can contribute additional amounts to these tax-advantaged savings accounts.

Jeremy Ney of American Inequality gives further insights into the poverty situation in the US.

The Expanded Child Tax Credit, enacted in 2021 for only 1 year, gave families with children approximately $3,000 to $3,600 annually per child.

This is a low estimate, as the “Trump Accounts” program allows families and employers to invest additional amounts in these “Trump Accounts”. As these are tax advantaged accounts, it is a subsidy that will be used mostly by higher income individuals (as they are likely to have extra savings as well as employers that would contribute to their “Trump Accounts”).

Connecticut created a policy where children are given a funded savings account, which they can access as adults, only after completing a financial literacy course.

While people concentrate on the future value of money aspect, it should be noted that the inflationary aspect of goods or services is getting cast aside. That dollar invested today will ultimately lose purchasing power.

The COVID Era subsidies were poorly designed as to the captured group and rushed payments that created debt where the interest payments outlast the effectiveness of the program.

With Trump Accounts we still don't know the fee structures or who will ultimately manage them.

If this were such a good idea, Congress wouldn't have allowed it to sunset in 2028. Just another boondoggle using other people's money...

I'm dubious of every new tax loophole. They are inevitably exploited by the rich (remember Romney's $100 million IRA built from contributions valued at a penny on the dollar?) and ensnare everyone else in labyrinthine tax code. If we want to help people then provide either money or services, not contrivances of the financial and insurance industries. Accounts that can be invested in equities boost asset prices, at least for a while. Subsidize education, not student debt; subsidize housing, not mortgages; subsidize healthcare, not health insurance.

I fear these minor savings accounts are also a move to rationalize coming cuts to Social Security as we approach the bankruptcy forecast in only 6 years. Raising the eligibility age will barely move the needle on solvency, but billionaires are desperate to distract from the policy changes that will make a difference: lift the cap on income taxed, and widen the types of personal income that are taxed for Social Security.