The Rise in Startup Fraud

Venture capital-backed firms have become more friendly to founders, but this, in turn, is leading to increased fraud.

Nominal News is an economics newsletter written by a PhD Economist that translates the latest economic research into clear, policy‑relevant insights on current issues. Join 4,000 readers to stay-up-to-date with Nominal News directly in your inbox:

Venture capital (VC) – a form of financing high risk/high reward early stage firms – has led to the creation of many large companies like WhatsApp, eBay, Uber, etc. Although VC investments can be highly lucrative, one of the main concerns of investing in early stage startups is the alignment of interests between investors and company founders, commonly referred to as the ‘principal-agent problem’. VC investments alleviate this problem through complex contracts1 between investors and founders. However, since the 2000s, changes in these contracts may have led to an increase in founder fraud. Dyck, Fang, Hebert and Xu (2026) (“DFHX”) took a closer look into this.

What is Venture Fraud and Why Should We Care?

Venture fraud occurs when the company, most often its founders, deliberately conducts fraudulent activity that harms the VC investor. This is often done when founders misrepresent financials (Spartan Micro), claim to have more customers than they do (Frank vs JP Morgan), or lie about what their product does (Theranos).

One could argue that venture fraud is a private matter since most damages occur between two private parties – investors and founders. There may even be an ‘optimal’ level of fraud, since to perfectly prevent fraud, investors would need to spend a lot of money and time to ensure fraud doesn’t occur, or simply undertake fewer investments. However, the effect of venture fraud may spillover more broadly into society, which then makes it a topic of interest.

The Case of Theranos

Theranos claimed to have designed a compact blood testing machine that, using a small amount of blood, would give quick results. Several US pharmacies planned to open in-store rapid blood testing using this product. However, it turned out that the machine was entirely fraudulent. This ended up hurting patients, who were misled by the tests. The damages to patients, as well as the wasted time/capital of pharmacies are specific social damages – commonly known in economics as negative externalities.

Investors, beyond their own financial windfall, do not take into account possible negative externalities – i.e. they do not internalize these negative externalities. This means that from a society perspective, venture fraud is more damaging than to the investor, and therefore, too much venture fraud occurs.

Preventing Fraud

The main way investors prevent fraud from occurring is by having control in the firm they invest in. This is usually done via having voting rights in the board of the firm. In this role, investors can vote on changing CEOs (who are often the original founders), as well as setting compensation structures for the CEOs. Company boards also approve or block key business decisions. Thus, investors may often want to have control of the board (i.e. more than 50% of the voting rights). But in the last few decades, this investor control appears to have reduced.

Causes of Venture Fraud

The Theories

DFHX posit three different hypotheses on what may make fraud more likely to occur:

Founder-friendly board structures – the original founders have more voting power in the boards of their companies, allowing them to mask fraud;

The number of investors in a firm has increased – each new investor in a board may have a different goal (company growth vs. cash distributions to investors) leading to more board disagreements, which in turn reduce the quality of oversight in a firm, allowing fraud to occur;

Founder characteristics – certain traits of founders, whether innate or developed over time, can lead to fraud occurring more often.

DFHX also looked at whether market conditions mattered for fraud. DFHX hypothesized that under “Hot Markets” – if macroeconomic conditions are such that firm valuations are higher, board control may be weaker, as investors are not as focused on company control. Moreover, there may be more investors in the market, competing for a limited pool of founders, which in turn allows founders to have friendlier board structures.

Data Collection

To test the theories, DFHX turned to data. The data collection process here is actually quite interesting, as there is no simple data set that can be easily looked into. DFHX looked at several sources – Securities and Exchange Commission (SEC) and US Department of Justice (DOJ) official filings, a Class Action lawsuits database, the Westlaw research platform and the Pitchbook investments news data feed.

The main issue for DFHX with data collection is the concern of not capturing all venture capital fraud events. This can skew the results if, for example, only specific venture fraud cases are reported. That is why DFHX looked at multiple databases to capture as many fraud cases as possible. Overall, DFHX built a sample of 614 US based venture fraud cases since 2000.2

Now, to study if venture-capital backed firms are more or less likely to have fraud cases, DFHX looked at a sample of 4,094 VC-backed firms and non-VC-backed firms that had an Initial Public Offering (IPO). IPOs (being listed on the stock market) have stringent disclosure requirements; often, fraud gets discovered in this phase. The fraud discovered during the IPO (or soon after it) can be assumed to have been caused by the company’s management team (i.e. often the founder) prior to the IPO.

Separately, to study what may be driving the differences in fraud level amongst venture capital firms, DFHX looked at a sample of 78,852 VC-backed firms in the 2000-2020 time period.

Predictors of Venture Fraud – Results

DFHX found that VC-backed firms that IPO’d are 54% more likely to have committed fraud than non-VC backed firms. To put it into context, about 8% of firms that IPO’d had a fraud lawsuit, while the rate for VC-backed firms was closer to 12-13%.

When looking specifically at VC-funded firms (not necessarily IPO’d), DFHX found that companies where the founder has control over the board are 88% more likely to commit fraud. Moreover, every additional investor on the board increases fraud likelihood by 8%. If the investors are less involved in oversight, like mutual funds or hedge funds who do not actively participate in board meetings, fraud is also more prevalent.

When looking at founder characteristics (age, gender, education, etc.), DFHX found that these did not matter for the likelihood of fraud. What did matter is whether the market was ‘hot’ when the VC funding round happened. That’s most likely driven by the fact that investors offered founder-friendly terms during these times, as there were more investors chasing fewer founders.

Lastly, one additional question DFHX looked at is whether fraud-involved founders are ‘disciplined’ by the market. Typically, one would assume that if someone committed fraud, this person would be less likely to receive investment in the future. Surprisingly, DFHX found that there is no market discipline – founders that committed fraud are just as likely to receive investment in the future as founders that did not.

Dealing With Fraud

The DFHX paper has several interesting implications. First, it shows the importance of the often-studied topic in economics of the principal-agent problem. The reduction in oversight by investors appears to have led to a real increase in fraud by founders (shown in next section below). It also shows the weakness of market mechanisms, as it appears that the market is not discipling fraudulent founders. This is a surprising result, as a common argument against regulations is that market actors will self-discipline. Here, it appears that investors are willing to take unnecessary losses.3

Regulatory Scope and The AI Boom

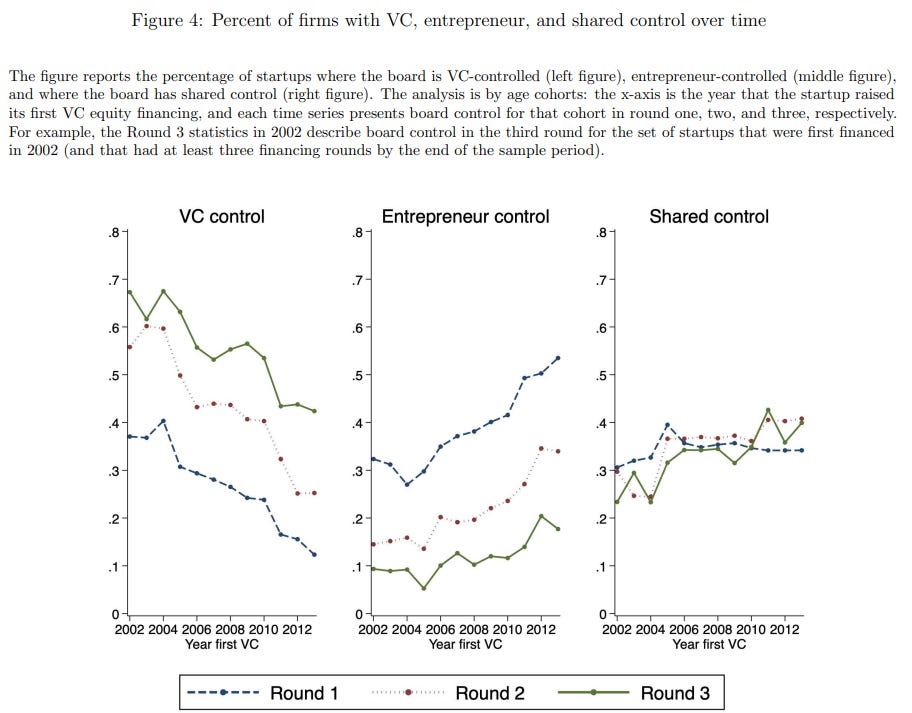

If we look at the VC market today, it appears that we’re in a ‘hot’ genAI market. Based on the DFHX research, this suggests that in the future, we may see quite a bit more fraud than usual associated with these VC-backed investments. As shown here by Ewens and Malenko (2020), founder/entrepreneur control has gone up over time at every stage of the company’s financial lifecycle in recent years (lines specify which round of fundraising it was):

It’s worth noting that, historically, founders rarely had 50% control after the first round of funding, as can be seen in the middle chart.

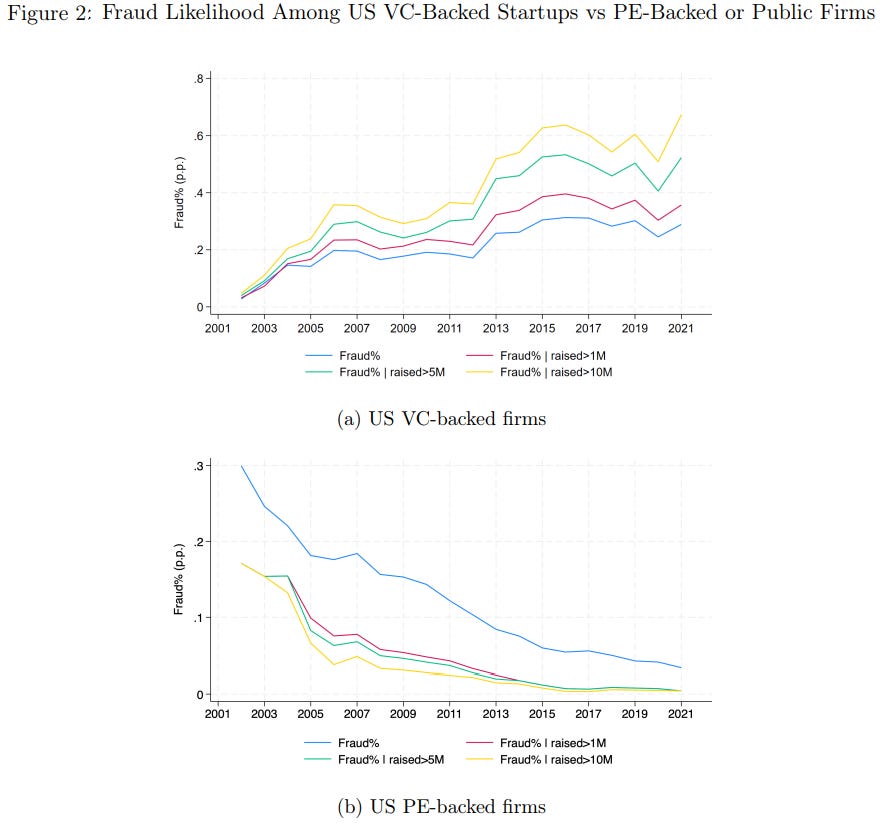

It is worth noting, that in other contexts, such as in the Private Equity-backed companies, DFHX found that fraud has not increased, and actually declined, clearly showing that oversight by investors, specifically in the VC space, is lacking:

From a policy perspective, it may make sense for governments to enhance oversight over VC-backed companies by potentially increasing financial reporting requirements, as VC investors appear to be more tolerant of fraud than socially optimal. This suggests that there may be scope for regulations to correct this market inefficiency.

Let me know your thoughts on this topic and whether you think intervention may be needed to reduce the amount of fraud.

If you would like to support us in reaching our subscriber goal of 7,000 subscribers, please consider sharing this article and pressing the like❤️ button at top or bottom of this article!

Interesting Reads from the Week

A Simple Idea That Could Change Things for Kids: Child Impact Statements – Bruce Lesley provides an interesting idea of requiring policy changes to have a ‘child impact statement’: that is, an explicit statement on how this policy change will impact children.

Does Where You’re Born Matter More Than How Hard You Work? – Abdullah Al Bahrani discussed why it appears that the physical location where one grows up explains a large amount of a person’s outcome: “Roughly 60 percent of the variation in outcomes across neighborhoods reflects genuine causal effects of place – not just differences in the families who happen to live there.”

Note: An economics professor argues that economists should not come up with solutions. That is not something I agree with – as discussed in our article a few weeks ago.

For example, control of the firm can depend on the external debt capacity of the firm – the less a firm can raise in debt capital, the more control a venture capitalist should have. This type of structure was modeled by economists – Aghion and Bolton (1992). Aghion is the recent (2025) Nobel Prize winner in economics.

The sample consists of cases that were both ruled on by courts and dismissed by courts. The reason why the dismissed court cases were also included is due to the fact that dismissals often occur due to procedural reasons – for example, the parties did not go to the correct arbitrating bodies first, before going to court. This dismissal does not mean fraud did not occur.

The DFHX paper lines up interestingly with a paper we covered a few years ago here – Davenport (2022) found that VCs could increase their returns by using a simple algorithm to prune out bad investments. One reason for these ‘predictably bad investments’ was that VCs over-valued founder backgrounds. The DFHX paper perhaps puts a different perspective on this question – if as a VC, you are friendlier to the founder, you are more likely to be defrauded resulting in these ‘predictable’ losses.

Here is an unusual example of fraud that actually provided benefits to society: "Mary Beth Combs argues that the English Parliament passed married women’s property legislation in 1870 not out of concern for wives’ well-being, but out of a desire to appease creditors by making wives jointly responsible (with husbands) for family debts."

https://digitalcommons.osgoode.yorku.ca/cgi/viewcontent.cgi?article=2808&context=ohlj

(Unfortunately I do not know of a digital version of this that I can share, but it's a cool paper.)

Effectively she argues that a large reason that the first married women's property laws were passed in England was bc husbands and wives were legally separating/ divorcing and the husband was giving the wife all (most of) the property at the time of divorce in order to shield their family assets from creditors. But, they would remain together even though they were legally separated/ divorced. Mary Beth argues that the fraudulent practice became so common that passing the MWPA was a compromise where wives were given expanded property rights but also made liable for their husbands debt's. Adding debt responsibility for wives gave them enough votes to get previously failed married women property legislation passed through Parliament.

Why would more investors on the board increase fraud likelihood?

If there is a good solution for the fraud probem, does it really need to be a govt regulation? How about a product that VCs could use to better investigate founders for fraud backgrounds or similar?